Country-by-country reporting (CbCR) was introduced in October 2015 under the Final Report on Action 13 of the Organization for Economic Cooperation and Development’s (OECD) Base Erosion and Profit Shifting (BEPS) Project. CbCR is designed as an assessment tool for high-level transfer pricing risks posed by large multinational enterprise (MNE) groups. It may also be used by tax administrations in evaluating other BEPS related risks.

Since 2016, many jurisdictions have implemented CbCR. Hong Kong introduced its own requirements under the Inland Revenue (Amendment) (No. 6) Ordinance 2018 (the amendment ordinance). Constituent entities (CEs) of “Reportable Groups” (RG) in Hong Kong (HK-CEs) must comply with the rules for financial periods beginning on or after 1 January 2018 (FY2018). Failure to comply could attract potentially heavy penalties.

The report

A country-by-country (CbC) report consists of three tables:

- Table 1 requires aggregate tax jurisdiction-wide information relating to the global allocation of income, profit, taxes paid, and certain indicators of the location of economic activity among tax jurisdictions in which the MNE group operates.

- Table 2 requires a listing of all the CEs of the MNE for which financial information is reported and the nature of the main business activities carried out by each CE. This is done by checking one (or more) of the 13 prescribed categories which include research and development, manufacturing or production, sales, marketing or distribution, etc.

- Table 3 enables a MNE to provide additional information or explanation that is considered necessary, or that would facilitate the understanding of the compulsory information provided in tables 1 and 2.

Reportable Groups, CbC notifications and CbCR filing

Usually it should be relatively easy to determine if an entity is required to file a tax return or not. This is not the case for CbCR. A MNE is considered an “RG” for a period if its total consolidated group revenue in the preceding fiscal year exceeds a threshold level. For Hong Kong-domiciled groups this is revenue of at least HK$6.8 billion, with the first implementation year of FY2018. Therefore, if a Hong Kong MNE reported revenue of HK$7 billion in FY2017 it would need to file a CbC report for FY2018.

If the MNE’s ultimate parent entity (UPE) is a tax resident in a jurisdiction other than Hong Kong, the MNE must follow the reporting requirements of that jurisdiction, or the default reporting threshold of €750 million (roughly HK$6.6 billion).

If the RG’s UPE is a Hong Kong tax resident (HK-UPE), the UPE shall file the CbC notifications with the Hong Kong Inland Revenue Department (IRD) within three months after their financial year-end. If the UPE is a tax resident in another jurisdiction they may appoint a HK-CE as the “surrogate parent entity” (HK-SPE). A SPE is the sole-substitute of the UPE for the filing of the CbC reports on behalf of the group in the tax jurisdiction where the SPE is a resident. If a HK-SPE is appointed they shall file the CbC notification on behalf of all of the group’s Hong Kong operations. Otherwise, HK-CEs can file CbC notifications independently or on behalf of other CEs of the group.

If the UPE or SPE is not a Hong Kong tax resident, the filing obligation falls on the HK-CEs as a local filing unless the IRD is able to obtain the MNE’s CbC reports via exchange mechanisms in place with other jurisdictions. Whomever is the reporting entity (HK-UPE, HK-SPE or HK-CEs), they must file the CbC report with the IRD within 12 months after the year-end.

The above is related to the notification and filing of CbCR in Hong Kong. RGs have to manage the same process in all the jurisdictions they operate and meet any other specific local requirements.

The exchange mechanism

Automatic exchange of CbC reports with other jurisdictions is achieved based on an international agreement – the Multilateral Competent Authority Agreement on the Exchange of CbC Reports (MCAA). Hong Kong signed the MCAA in 2018 and as of June 2019, 56 bilateral exchange relationships have been activated. However, there is a catch: for Hong Kong the exchange relationship under the MCAA are effective for taxable periods starting on or after 1 January 2019.

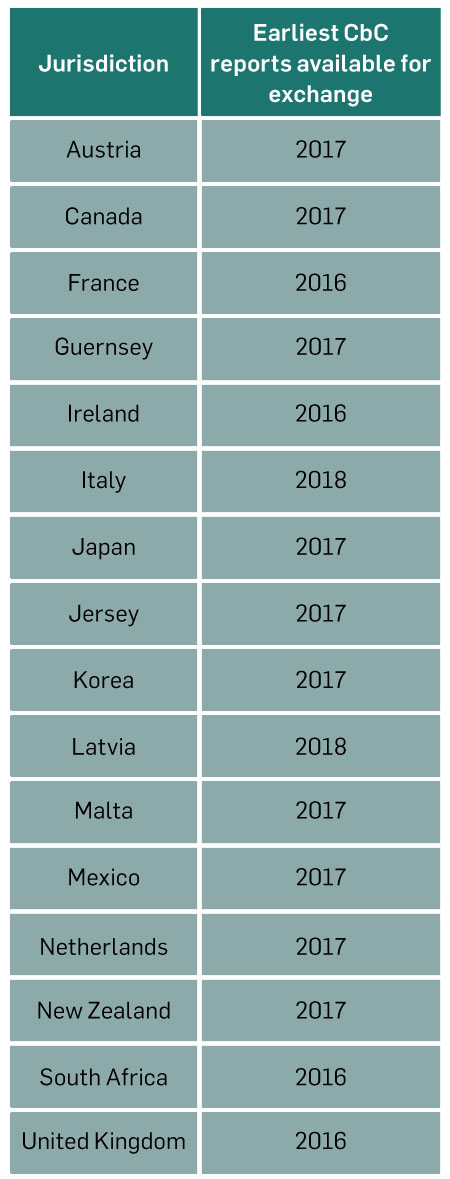

What does it mean for CbCR filing for FY2018? As of June 2019, Hong Kong has signed bilateral CbC exchange agreements with 16 jurisdictions (see the table) to facilitate CbC report exchanges for earlier periods.

Jurisdictions Hong Kong has bilateral CbC exchange agreements with.

.

For a foreign RG with HK-CEs, local filing for FY2018 by the HK-CEs would be inevitable – unless the UPE or SPE is a tax resident in one of the 16 jurisdictions and other conditions in the amendment ordinance are satisfied. If so the IRD can obtain the FY2018 CbC reports filed from these jurisdictions. From FY2019 onwards, the IRD is able to obtain reports from the 56 jurisdictions (or more), and a local filing may not be required.

Many foreign RGs are MNEs based in the United States. The U.S. did not sign the MCAA but instead arranged bilateral exchange agreements with other jurisdictions. Before the U.S. and Hong Kong conclude the bilateral agreement, local filings by the HK-CE of large U.S. MNEs will be required, unless the IRD can obtain CbC reports through a SPE that resides in a tax jurisdiction with which Hong Kong has a bilateral exchange relationship.

Preparation of the CbC report

RGs with operations in many jurisdictions would most likely have been preparing CbC reports for FY2016 and FY2017, and the local filing in Hong Kong would thus be an additional piece of reporting which does not involve tax calculations or liabilities.

Now that RGs must prepare CbC reports for the first time for filing in Hong Kong they should follow the rules in the amendment ordinance and the OECD Action 13. To help them, the OECD has issued the following guidance the Guidance on the Implementation of CbCR (last updated September 2018) and the CbCR: Handbook on Effective Implementation (2017).

Preparation of CbC reports is not rocket science. It is a process of gathering data and factual information. However, MNEs need to decide on their position to take in the CbC report and ensure that all CEs follow the same position consistently year-on-year. Each step also requires careful planning and execution in order to meet filing deadlines. Needless to say, the more CEs across different jurisdictions, the more difficult it will be to manage the process and the risk of error will increase. Training and strong project management are critical for completing CbC reports on time.

In addition, although MNEs are given 12 months to prepare the CbC report, when they can actually commence data input depends on how long it takes to finalize their financial statements. The longer it takes to finalize the accounts, the less time there is to prepare the CbC report. For many, the time available would likely be less than nine months.

The CbC reporting portal

In Hong Kong, CbC notifications and CbC reports must be filed via the CbC reporting portal. To do so, the HK-CE must register a CbC reporting account through the portal. The person authorized to register a CbC reporting account for the HK-CE has to apply for an e-Cert (Organizational) with automatic exchange of financial account information functions (e-Cert) from Hongkong Post for authentication purposes.

Similar to most tax jurisdictions, a CbC report must be in the form of an XML document for submission to the IRD. To assist, the IRD has developed a data schema in XML which is based on the CbC XML Schema v1.0.1 issued by the OECD. The data schema specifies the data structure and format for filing CbC report. The data schema and a related user guide are available on the IRD website for download.

Records keeping

Section 58L of the amendment ordinance requires that a “reporting entity” must (a) keep sufficient records to enable the accuracy and completeness of the CbC report to be readily ascertained; and (b) retain the records for a period of six years beginning on the date on which the return is filed. The burden on the reporting entity is indeed substantial and thus it is important to know which entity is the reporting entity.

Under section 58J of the amendment ordinance, a reporting entity includes the Hong Kong entity that is required to file a CbC return (i.e. the HK-UPE, HK-SPE or HK-CE) and any HK-CE that is required to file CbC notifications.

The record keeping obligation imposed on the HK-SPE or HK-CEs is somewhat burdensome. For example, a United Kingdom-based MNE with global operations would normally not allow the management team of the subsidiary (the HK-CE) to have access to financial information of the group entities outside their management responsibilities. The HK-CE would only have CbC notification obligation in Hong Kong (as the IRD can obtain the group CbC report from the U.K.’s Her Majesty’s Revenue and Customs via the exchange mechanism). Yet, section 58L requires the HK-CE to maintain sufficient records for six years to enable the accuracy and completeness of the group’s CbC report be ascertained.

Penalties

Division 6 of Part 9A of the amendment Ordinance contains the penalty provisions for CbCR. The new section 80G provides that a reporting entity commits an offence if the entity, without reasonable excuse, fails to file a CbC notification, or CbC report, or keep records as required under section 58L. That reporting entity would be liable on conviction to a fine at level 5 (HK$50,000), and the court may order the entity to complete the act it failed to do, within a specified time frame. The reporting entity is liable to a further fine of HK$500 for every day or part of a day during which it fails to file the CbC notification or CbC report.

Obviously, there are further penalty provisions, including imprisonment for three years, for more serious offences.

Concluding comments

CbCR is a very unique tax filing. There is no tax to be calculated and no money to be paid, the “taxpayer” can in some cases choose where to file it but needs to comply with all the CbCR rules and regulations in all jurisdictions that they operate in, and corporate restructuring or mergers and acquisitions could bring chaos to the notification and filing. In an acquisition, the buyer will need to obtain warranties or indemnities from the seller for exposures relating to CbCR. Compliance with records keeping obligations may also create tension between the buyer and seller.

With all the complexities, jurisdictions should implement the CbCR rules in a lenient manner, thereby reducing the pain felt by businesses. For instance, Singapore only accepts UPE filing (i.e. MNE whose UPE is a Singapore tax resident, and no surrogate parent or local filing is accepted) and the local tax office would inform the UPE that they need to file the CbCR. In addition, Singapore’s CbCR filing is done by sending the CbC report in XML format to the Inland Revenue Authority of Singapore via email.

Unfortunately, Hong Kong has taken a very different approach, which may erode Hong Kong’s reputation as a friendly international business centre.

Readers should note that the objective of this article is to highlight the key provisions in the CbCR rules. For completeness, readers are advised to seek professional assistance to enhance their understanding of the rules, their obligations and the penalty provisions.

Edwin Bin is Managing Director of Manage Your Tax Company Limited