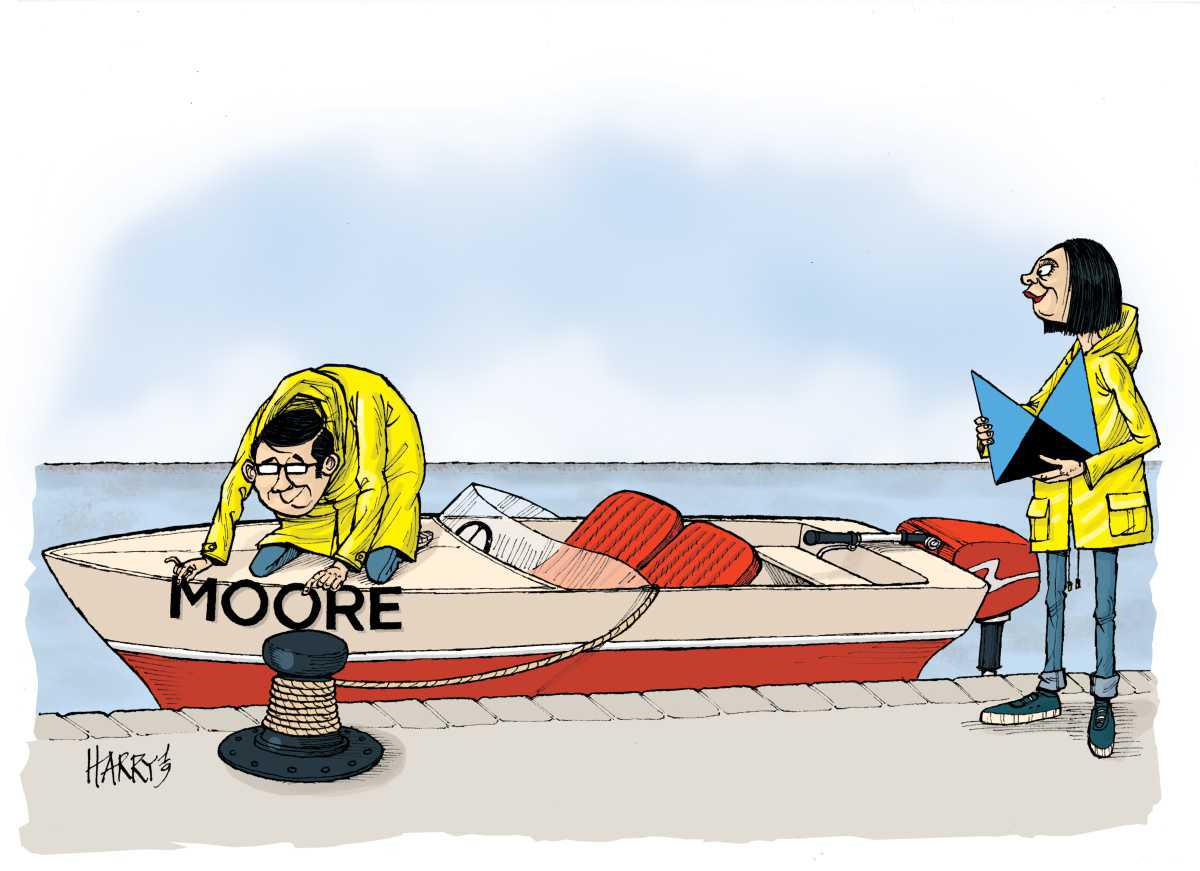

Moore Stephens changes name

Moore Stephens International has rebranded its name to “Moore.” The move, which took place on 9 September, is part of the firm’s initiative to “encapsulate the traditional core strengths of Moore Stephens, while positioning a more modern, internationally relevant brand, supporting the future success of a globally connected accounting and consultancy network.” The change, which applies to Moore Hong Kong, also includes a new logo, visual identity and motto: “Helping you thrive in a changing world.” Most of the firm’s 260-plus independent member firms with adopt the new brand by mid-2020. “With our new brand – Moore – we choose a new identity fit for a world defined by global decision-making, data-driven insight and the need for agility in all that we do,” said the Chief Executive Officer of Moore Global, Anton Colella.

KPMG to handle Thomas Cook collapse

KPMG have been appointed to deal with the liquidation process of travel company Thomas Cook, which collapsed on 23 September, after a last-minute effort to recapitalize failed. The collapse of the 178-year-old group has impacted more than 20,000 jobs, including 9,000 in the United Kingdom, and the Department for Transport and the Civil Aviation Authority are tasked with getting 150,000 stranded holidaymakers back to the U.K. Experts in insolvency have been called in to manage the liquidation of the group’s retail and engineering departments. “The immediate priority is to provide support and assistance to those employees who have been made redundant,” a KPMG spokeswoman said.

Accounting groups meet at New York Climate Week

International accounting groups gathered in New York on 23 September to address the risks of climate change. The International Federation of Accountants (IFAC) hosted a panel discussion along with the Association of Chartered Certified Accountants to discuss the role of the accounting profession in responding to calls for more rigorous environmental, social and governance reporting and sustainability practices. The panel included sustainability experts from Big Four firm Deloitte, technology companies Salesforce and Datamaran, the World Business Council for Sustainable Development, and the Financial Times. Chief Executive Officer of IFAC Kevin Dancey introduced the panel, saying: “Climate change is a very serious issue. This is one big, scary, global multifaceted societal problem. There is no long-term planning horizon. The threat to economic and financial stability is here and now. There’s really just no time.”

Gucci executives probed over tax evasion claims

Italian authorities are investigating more than a dozen current and former executives of luxury label Gucci. Gucci’s headquarters in Florence and Milan were audited in 2017 amid allegations that the brand fed revenue through Switzerland to avoid paying Italy’s higher tax rates. The investigation appeared to reach a conclusion in May when Gucci parent Kering handed over US$1.4 billion in unpaid taxes. The Italian government has widened its probe and is now investigating individual managers’ pay from 2011 to 2017. According to Bloomberg, the executives could owe tens of millions of dollars in back taxes. The investigation is in its early stages, with no criminal inquiries opened at present.

78% of internal auditors cite cybersecurity as biggest concern

Cybersecurity tops the list of concerns for internal audi- tors this year, according to a collaborative report by eight European institutes of internal auditors. The report noted that 78 percent of internal auditors across Belgium, France, Germany, Italy, the Netherlands, Spain, Sweden and the United Kingdom view cyber attacks to be the biggest risk facing businesses. This has led to more accounting firms recruiting experts in cybersecurity due to the large amounts of financial information they have access to. According to job website Indeed, one in every 17 recruits to KPMG is for a cybersecurity role, and in 2018, Deloitte spent US$580 million on improving its cybersecurity capabilities.

London Stock Exchange rejects US$37 billion takeover bid made by HKEX

The London Stock Exchange (LSE) has turned down a US$37 billion acquisition offer made by the Hong Kong Exchanges and Clearing (HKEX). In a statement issued on 13 September, the LSE’s board unanimously rejected the conditional proposal from the HKEX, saying that it was too low, lacked strategic merit and was politically risky. It also said it remained committed to its acquisition of financial data provider Refinitiv, even though the offer by the HKEX, the highest ever takeover offer for a stock exchange, was conditional on the LSE axing its proposed acquisition. HKEX has vowed to continue its pursuit despite LSE’s focus on the separate transaction.

Money-laundering regulator closely watching Facebook’s Libra

The global money-laundering watchdog is keeping an eye on Facebook’s planned cryptocurrency, Libra, in the latest sign of growing scrutiny against the project. The virtual currency, which is due to launch in June 2020, will work as a blockchain-based digital coin allowing Facebook users send and receive money or to pay for services. “We want to make sure that if there are significant risks, they need to be addressed,” said Xiangmin Liu, President of the Paris-based Financial Action Task Force. Regulators have voiced concerns that it could be used to upset financial stability, and a senior U.S. Treasury official has stressed that the currency must meet the highest standards in fighting money laundering if it is to receive the green light.

Media metrics giant charged with fraud

Comscore, an analytics company that measures web traffic, has been charged by the Securities and Exchange Commission (SEC) for falsely reporting its own revenue and customer numbers. Former chief executive officer of Comscore, Serge Matta, has agreed to settle the case for a total of US$5.7 million without admitting wrongdoing. The SEC alleges that between 2014 and 2016, Comscore added US$50 million to its public revenue filings by misreporting the value of data-swapping contracts with other companies. Matta, who resigned from the company in 2016, will also repay US$2.1 million to Comscore and be banned from serving as an officer or director of a public company for 10 years.

U.K. Big Four commit to disability inclusion

Deloitte, KPMG, PwC and EY in the United Kingdom have signed onto a disability campaign, The Valuable 500, supporting inclusivity in the business world and marking a collaboration in the first of its kind. The Valuable 500 is a global movement that partners with the private sector to create disability diversity in the workplace. Each firm will now be held accountable for disability inclusion, partly by ensuring it is discussed by board-level leaders and action is taken as a result. “Diversity and inclusion is part of the lifeblood of our organization and we believe that we all need to work together across the globe to bring more attention to this important issue,” said Chief Executive Officer of EY, Carmine di Sibio.

U.K. companies need more time for lease standards

Only 26.3 percent of public companies have implemented the use of the new lease accounting standard, despite the effective date of 15 December 2018, according to a Deloitte survey. Though many public companies have already used the new standard in one reporting period, many of them have not implemented the new leases standard. “Most of our U.S. public company clients have completed initial compliance activities, but very few have fully completed their broader lease implementation efforts,” said Deloitte Risk & Financial Advisory Managing Director Sean Torr in a statement.

Peloton prices its IPO

Exercise bike and treadmill company Peloton priced its initial public offering (IPO) at US$29 a share. The offering raised US$1.16 billion, valuing the company at US$8.2 billion. It began trading on the Nasdaq stock exchange on 26 September under the ticker PTON and subsequently fell by 11 percent. Though Peloton’s revenue doubled to US$915 million, the listing comes amid losses, which saw the company accumulate losses totalling US$196 million during the first two quarters of the year. It is also facing a US$300 million lawsuit from a group of music publishers who accuse the company of using more than 2,000 songs in its workouts without paying licensing fees.