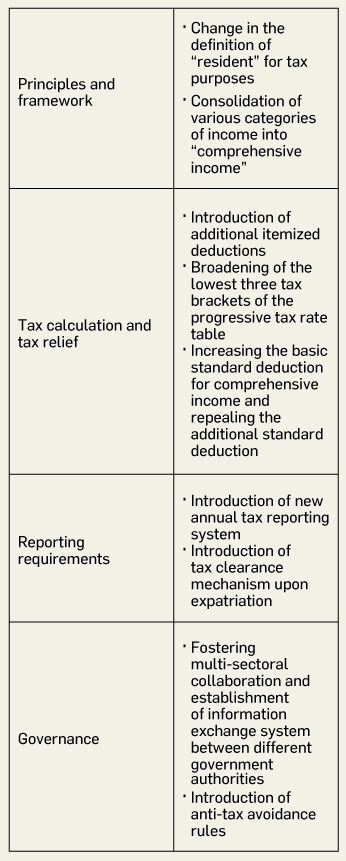

The National People’s Congress of the People’s Republic of China released draft amendments to the Individual Income Tax (IIT) law for public consultation from 29 June to 28 July. The overwhelming response rate of over 130,000 submissions received within one month is an indication that the public and various stakeholders have high awareness and interest in the proposed amendments. The key changes included in the draft are:

If these proposals become effective, there could be substantial impacts on taxpayers. At the same time, implementation of the proposed amendments will bring changes to the tax exposures of almost all IIT payers and potentially bring more people into the tax net. Furthermore, there are also implications on the tax reporting mechanism.

Any implementation of the proposed amendments would therefore impact the existing IIT framework. While the China IIT law forms the backbone of the tax framework, interpretation and execution of the IIT law effectively relies upon sets of circulars issued by the tax bureaux from time to time. As a result of implementation of the proposed changes, some of these circulars will no longer synchronize with the revised IIT law. However, it is still uncertain how these circulars will be updated along with the revised IIT law, or, for some circulars, be abandoned. Notable examples of circulars likely to need amendment or removal include preferential tax treatment on bonus and equity income, time apportionment claim, and the “five-year” rule.

If the amendments are approved, the new IIT law should become effective on 1 January 2019, although some measures will take effect as early as 1 October 2018.

In this article, the implications of the revised IIT regime for the following stakeholder groups will be discussed:

- Local Chinese employees

- Foreign employees working in China

- High net worth individuals

- Employers

Local Chinese employees

Until now, IIT calculations on employment income are still a rather mechanical exercise performed by the employers, where the employers also act as withholding agents for tax reporting and payment purposes. Taxpayers’ personal circumstances and expenditures are rather irrelevant in the calculation. In order to promote social fairness and increase equality in tax treatment, China introduced a tax preferential treatment on commercial health insurance contribution scheme in 2015, and tax deferral on commercial pension insurance contributions (pilot) scheme in 2018. These schemes represented a new development in personal taxation, and formed the foundation of the personal tax relief introduced in these proposed amendments to the IIT law.

The proposed amendments also include the introduction of deduction for certain living expenses, e.g. child education, continuing education, medical expenses for critical illnesses, home mortgage interest, and housing rent. These items account for a significant portion of expenditure for the typical middle-class taxpayer. More importantly, these new measures will bring personal circumstances into consideration when calculating the IIT liabilities of the taxpayer. Specific details of the deductions, such as eligibility of expenses and the amount of allowable deductions, are yet to be announced.

The proposals also include broadening the three progressive tax brackets, at the bottom end of the progressive rate tax table, for comprehensive income (which currently apply to salaries and wages only). This would effectively lead to tax savings for the majority of the working population.

The standard deduction for local Chinese will also be increased from RMB3,500 per month to RMB5,000 per month.

Broadly speaking, the proposed amendments bring positive impacts to local Chinese taxpayers as their IIT burdens will likely be reduced.

Foreign employees working in China

On the positive side, foreign employees can also enjoy the bene ts of the broadening of tax brackets at the bottom end of the progressive tax rate table for comprehensive income, and the increased standard deductions from RMB4,800 to RMB5,000 per month.

Changes to residency rule

Despite the above, there is potential bad news for foreign employees which may outweigh the benefits. Currently, foreign individuals spending a “full year” in China are regarded as China tax residents for the year. A non-China-domiciled individual is regarded as having stayed in China for a full year if he does not physically leave China for more than 30 days in one single trip or for more than 90 days cumulatively in the calendar year concerned. For this purpose, both the arrival and departure days are normally excluded from the counting of the 30/90 days thresholds and it does not matter whether the overseas days are for personal or business purpose. Practically speaking, most foreign nationals are considered as non-China-domiciled individuals. However, they will only be subject to worldwide taxation in China if they spend a “full year” after they spend five consecutive “full years” in China (known as the five-year rule).

The definition of “full year” is therefore complicated. In short, a foreign individual will not be regarded as a China tax resident if he/she spends no more than 274 days in China in a calendar year. The proposed amendments shorten this window to 183 days. Foreign employees who work in China, especially those who work full-time in China, would easily become China tax residents according to the proposed amendments, even if they spend most of their weekends and holidays outside China (a common tactic for reducing tax liabilities). We suspect that the five-year rule will be removed so as to align with international practices, yet, the draft amendment is silent as to whether the five-year rule would remain.

Example

Assuming that a Hong Kong employee is seconded to work in an entity situated in China for 4 days per week. He spends 208 days in China every year (4 days x 52 weeks). The tax authority has already agreed that he can pay IIT on a time-apportionment basis. With the implementation of the proposed amendments, he would become a China tax resident and be subject to IIT based on his entire employment income. If the five-year rule is also removed, he will be subject to worldwide taxation in China, meaning that his other sources of income outside China (e.g. rental income, capital gains, dividends, etc.) could be subject to IIT.

Furthermore, according to the prevailing Hong Kong Salaries Tax rules, the individual could enjoy either a double tax relief pursuant to Section 8(1A)(c) of the Inland Revenue Ordinance or a foreign tax credit pursuant to the China-Hong Kong double tax arrangement, depending on his Hong Kong tax residency. Under either circumstances, relief will likely be limited to income attributable to his China work days. His income attributable to Hong Kong work days would then be subject to double taxation in China and Hong Kong.

To avoid unexpected double taxation, the Hong Kong employee and his employer should closely monitor the development of the IIT law amendment. Once the IIT law is amended, they should promptly revisit the individual’s tax residency status, travel patterns and staff deployment arrangements to ensure tax efficiency can be achieved.

IIT on fringe benefits

It is worth noting that the proposed amendments are silent on whether the non-taxable treatment for certain fringe bene ts made to foreign individuals, such as housing bene t, child education, will be removed and replaced by the deduction of certain living expenses applicable to all residents receiving comprehensive income. The likelihood is that they will be removed as the favourable tax treatment is not consistent with the intention to treat local Chinese and foreign individuals equally.

High net worth individuals

High net worth individuals (HNWIs) in China tend to be business/asset owners whose main income streams are from dividends, pro t distribution, and income from leasing or transferring properties. Though the proposed amendments do not change the IIT treatment of these income categories, the newly proposed general anti-avoidance rule (GAAR) may still impact HNWI. Taking the example of disposal of a business, instead of a direct disposal, the owner may enter into a series of transactions that are not on an arms-length basis, with the view to be taxed at a different rate or to take advantage of double tax treaty protections. The proposed GAAR may prompt the owner to reconsider whether the planned transactions remain sustainable upon challenge.

Another observation is that these HNWIs often, at some stage in their life, consider migrating to another country/ territory. As soon as they obtained overseas permanent residency, they could apply for the household registration (or Hukou) to be deregistered. With the tax clearance procedure introduced by the proposed amendments, these HNWIs will need to understand what this means to them, in particular any “dry tax charges” on unrealized gains at the time of expatriation.

Even if they successfully deregister their Hukou, their ties with China may not be entirely eliminated. Many of them would retain their businesses in China and would frequently travel to China to manage their business. With the change of residency rule mentioned above, their income may still fall into the China tax net if, for example, they become China tax residents due to the length of time spent in China.

Employers

The proposed changes to the tax reporting system are meant to reduce the tax compliance burden on employers acting as tax withholding agents for employment income. Under the proposed amendments for tax resident employees, employers are only required to withhold an estimated IIT in respect of their tax resident employees from their payroll on a monthly basis. This approach is in line with many other sophisticated tax jurisdictions, and might ease employers’ workload when compared to requiring an accurate IIT withholding as is currently the case.

However, we suspect that the reality may be the reverse. With only the estimated IIT withheld, the tax authorities expect taxpayers to le annual tax reconciliation schedules and either pay or be refunded a true-up amount. If a taxpayer fails to meet the reporting requirement or paying the tax undercharged, it is much easier for the tax authorities to go after the employer rather than the employee. On the other hand, over-withholding is not preferred either in light of the complex procedures to apply for tax refund, if it is in fact at all possible in practice. Employers are also concerned that any alleged non-compliance will be reflected in the newly established social credit information system, which may negatively impact the company’s reputation. Hence, we heard from many employers that they will take a wait-and-see approach and continue to withhold IIT on an accurate basis across the board.

What makes the IIT withholding process even more complex is the introduction of deductions for living expenses mentioned earlier. Taxpayers who wish to enjoy these deductions are required to submit the expense information to their employers as the withholding agent. This creates the requirement for a lot of communications between payroll/HR and their employees. Considering the already challenging monthly tax ling schedule, this additional workload will no doubt make the tax ling process even more challenging and time-consuming.

Companies should thoroughly review the developments in this area and any implementation guidelines. It may also become necessary to outsource the tax reporting function or to hire additional staff to meet the forthcoming changes.

Conclusion

This is the most comprehensive and forward-looking IIT law amendment since 1993, providing China with a sophisticated IIT framework. The implementation of the changes will be a challenge given the breadth and depth of these changes. With over 130,000 responses to the consultation, we suspect that implementation rules and supporting circulars will only be issued in phases. In other words, taxpayers and withholding agents will likely need to live with certain risks and uncertainties at the beginning of the rollout. Companies should consult tax professionals and keep abreast of the development in this area.

Finally, the IIT law amendment is good news to some, and not so promising for others. However, most would agree that the amendment does address the call of equality between local Chinese and foreigners, as well as differentiation among taxpayers with different personal circumstances.

Mona Mak is Partner and Kenneth Peh is Senior Manager of Deloitte Advisory (Hong Kong)