It’s now an apt time to review Mainland China’s Individual Income Tax (IIT) Reform, which has been in operation since the start of the year. Employers and withholding agents should have already completed the first monthly individual tax filings for January 2019 and will soon begin preparing their second monthly returns. It has been an exciting and challenging moment, especially for non-domiciled individuals (including people from Hong Kong) working in Mainland China.

In December 2018, just before the regime became effective, the State Administration of Taxation (SAT) issued eight regulations and notices concerning operational topics including tax collection and administration, self-declaration requirements, and withholding measures.

Improvements for residents

Under the new IIT rules, one of the key changes is to enhance taxpayers’ involvement in their own tax filing status. There are now several situations where a resident taxpayer would be required to conduct their own annual tax reconciliation (ATR), even though the withholding agent(s) has already withheld the IIT on a monthly basis. This means that the resident taxpayers would need to verify their own annual tax reporting status including but not limited to whether the tax withheld by the withholding agent is correct.

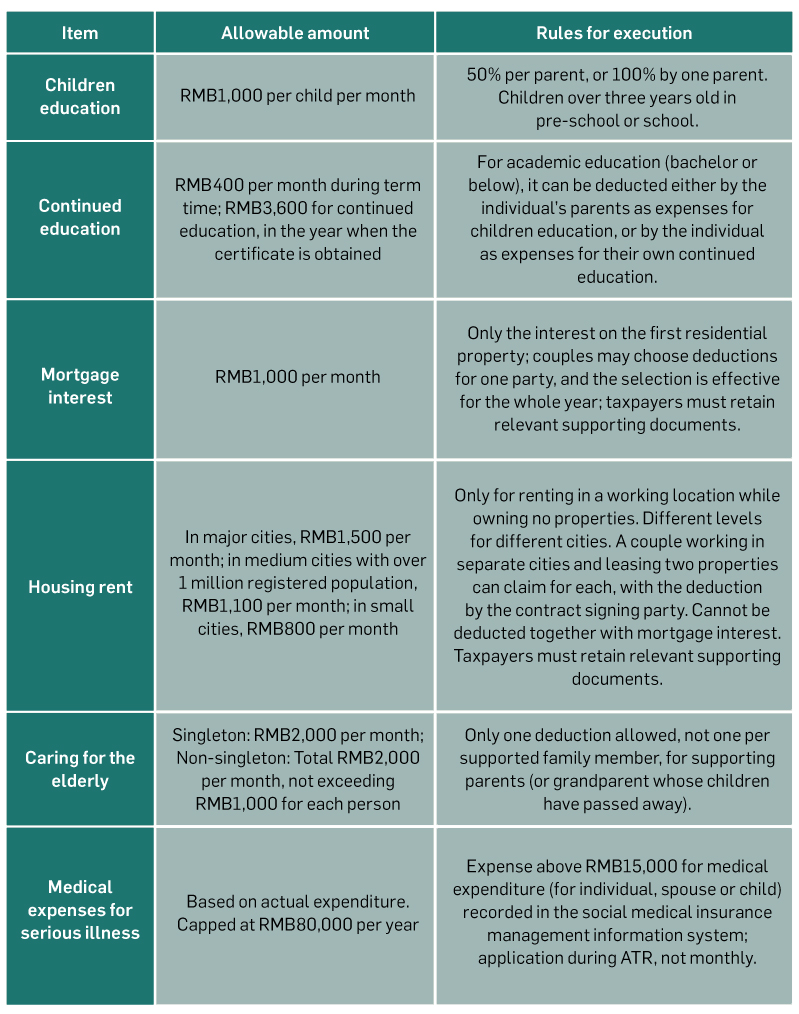

Another new eye-catching highlight is that resident taxpayers are now entitled to six newly introduced specific additional tax deductions (SATD), detailed in table below.

The introduction of the SATD is one of the most important developments in the IIT, and a breakthrough response to public calls for IIT reduction in light of personal finance and family burdens. In practice, resident taxpayers can request their employers (who are the IIT withholding agents) to deduct the respective SATD via the monthly pre-withholding (except for medical expenses for serious illness which must be claimed via ATR), or they can choose to claim deductions when they complete their ATR filing during March to June in the following year.

To assist taxpayers with their provision of SATD information, SAT has introduced a free web-based tool and mobile app to fill in the relevant information for claiming SATDs, as well as for the withholding agents to automatically download information on SATDs to complete the IIT pre-withholding process.

Questions for foreigners

While for residents the reforms are beneficial and appreciated, and respond to public concern, there are a number of questions for foreigners (including Hong Kong residents) working in Mainland China. The next section of this article considers five main questions for foreigners in relation to IIT.

Definition of tax resident’s “worldwide income” taxation basis

After the issuance of the new IIT law in August 2018, a commonly raised issue in the Hong Kong media was: will Hong Kong residents working in Mainland China be subject to “worldwide income” taxation basis once they have spent 183 days in Mainland China? This was a difficult question to answer, with many different opinions expressed, as the tax residency rule in Mainland China is quite complicated.

Technically speaking, an individual who has a “domicile” in Mainland China is subject to China IIT on worldwide income. “Domicile” means to habitually reside in Mainland China because of household registration, family and/or economic interests. For “non-domicile” individuals, if they physically spend 183 days or more in Mainland China, they will be treated as a “non-domicile” tax resident.

For “non-domicile” tax residents, in the new IIT regime a new “six year rule” replaces the previous “five year” tax break rule. This means that only when a “non-domicile” tax resident spends six consecutive years in Mainland China (i.e., 183 days or more in Mainland China each year) that they will be subject to China IIT on worldwide income. However, it is still possible to achieve a “tax break.” Under the previous IIT regime, a tax break could be achieved by leaving Mainland China for more than 30 days in one trip or more than 90 days in separate trips. Now, if at any time during the six year count, the individual leaves Mainland China on a single trip lasting more than 30 days within a calendar year, the count will reset.

Before a non-domiciled tax resident is taxed in Mainland China on his/her worldwide income, income which is both sourced AND paid/borne outside Mainland China could be exempt from IIT provided that a “registration” is filed with the tax authority in charge. We are still awaiting details of the registration requirement.

Example: Mr. Chan has been seconded from Hong Kong to Mainland China since 1 January 2014. He has been working full time in Mainland China without enough absence from the Mainland to have triggered a tax break under the previous IIT regime. 2019 is his sixth year in Mainland China and if he does not take a tax break in 2019, he would be subject to China IIT on his worldwide income starting on 1 January 2020. In order to avoid becoming a non-domiciled resident he would need to leave Mainland China for more than 30 days in 2019, which would reset his six year count.

IIT reporting method for tax residents vs. non-residents

The new IIT rule introduces different IIT filing requirements (including monthly withholding and year-end reconciliation) for tax residents and non-residents. For residents, IIT on their monthly employment income would be carried out by their employers (or relevant withholding agent) on a “pre-withholding” reporting of accumulated income basis. At the end of the tax year, the individuals need to perform an ATR (subject to certain exceptions) on their annual consolidated income (including employment income, income from independent services, royalty income, income from author’s remuneration, etc.). For non-residents, however, they cannot undertake ATRs. Instead, their IIT is reliant on accurate monthly withholding filings by their withholding agents.

This therefore leads to complications for withholding agents when choosing the IIT reporting method for non-domiciled individuals working in Mainland China, who may not be able to ascertain whether they would meet the 183 days in a year (therefore be treated as tax residents or not). For example, if the withholding agent adopts the “non-resident” IIT reporting basis in respect of a non-domiciled individual, but this individual ends up spending 183 days or more in Mainland China for that year (therefore becoming a tax resident), how should the withholding agent handle the IIT reporting basis? What are the administrative procedures for converting a non-resident to becoming a resident and which party should be responsible for any tax adjustment? The SAT is expected to issue further guideline on this.

Are there any double taxation implications?

No, the double taxation treaty, i.e. the arrangement between the Mainland of China and the Hong Kong SAR for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on income, is not affected by the new IIT law.

Future developments streamlining the IIT regime

Subsequent to the issuance of the IIT law in August 2018, there were rumours that the preferential calculation basis on annual bonus, equity incentives, as well as the non-taxable benefits items available to foreigners (under Guoshuifa [1997] No. 54) might be cancelled.

On 27 December 2018, the SAT issued circular Caishui [2018] No. 164 to provide a three year transition period (i.e., from 1 January 2019 to 31 December 2021) for, among other items, the tax calculation basis on annual bonus/equity income received by tax resident, and the non-taxable benefits treatment available to foreigners.

From 1 January 2022, annual bonuses will be included in an individual’s annual income and subject to IIT the same way as ordinary wages. For non-taxable benefits, three items, i.e. children education, housing, language training for foreigners will no longer be treated as non taxable. For the remaining non-taxable items such as meal and home leave, the non-taxable treatment may still be valid; however this is subject to further guideline from SAT. It is likely that for Hong Kong people working in Mainland China, the tax burden may be increased from 2022. Companies are recommended to analyse the possible impact and to evaluate available options concerning compensation design and/or future workforce resource plan in the Mainland.

Foreigner’s non-taxable benefits vs. SATD

There are overlapping items under the foreigner’s non-taxable benefits and SATD. The overlapping items include rental, children education and language training, although the criteria and quota are not identical.

Under the new IIT regime, tax residents (including domiciled residents and non- domiciled residents) are eligible to claim SATDs, while the foreigners are still able to claim non-taxable benefits. This means that some individuals (namely, foreigners who are tax residents) are eligible for both non-taxable benefits and SATDs. In this situation, the individual can only choose to claim one category.

Additional guidelines are necessary from SAT

While we are excited about the launch of the China IIT Reform, there are nevertheless many issues that are still unclear. We remain confident that these will be cleared up soon, maybe even before this article is published. These include:

- Whether beneficial tax calculations for annual bonus and equity will be applicable to non-residents? (Circular Caishui [2018] No. 164 only provides the transitional period for “tax residents.”)

- From 1 January 2022 onwards, non-taxable benefits for foreigners including housing, language training and children education will no longer be available. What about the meal/laundry and home leave?

- Will the time appointment calculation still be eligible for foreigners having regional roles?

Finally, while the SAT and relevant government bodies announced many regulations following the IIT reform, it is still an unavoidable fact that local tax bureaus may interpret the new IIT law (and relevant regulations) differently. Withholding agents and individual taxpayers are recommended to reach out to the local in-charge tax bureau to communicate on both the implementation details of the reform and the respective local interpretation.

.

Michael Hong and Tyrone Chan are Directors, People Advisory Services, at EY China. (This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Member firms of the global EY organization cannot accept responsibility for loss to any person relying on this article.)