In Hong Kong, entities without public accountability can choose to adopt the HKFRS for Private Entities Accounting Standard (HKFRS for PE), which is equivalent to the IFRS for SMEs Accounting Standard issued by the International Accounting Standards Board (IASB), for preparing their financial statements. The requirements in HKFRS for PE are based on those of the full HKFRS Accounting Standards, with simplifications to reflect the information needs of users of financial statements and the resources available to private entities. By relieving private entities of the requirement to apply the full HKFRS Accounting Standards, HKFRS for PE helps ease the reporting burden of eligible private entities that are not eligible to apply the cost-based home-grown Small and Medium-sized Entity Financial Reporting Framework and Financial Reporting Standard.

In September 2022, the IASB published an exposure draft proposing amendments to the IFRS for SMEs Accounting Standard, aiming to reflect the improvements made to the full IFRS Accounting Standards while keeping the standard simple. Key proposals include aligning certain requirements in the standard with those in International Financial Reporting Standard (IFRS) 9 Financial Instruments and IFRS 15 Revenue from Contracts with Customers. In response, the Institute submitted a comment letter to the IASB.

After several rounds of deliberation on the feedback, in February 2025, the IASB published the third edition of the IFRS for SMEs Accounting Standard. The Institute noted that our comments were addressed in the revised standard. Following the completion of the due process, the Institute issued the revised HKFRS for PE in April 2025, which is equivalent to the third edition of the IFRS for SMEs Accounting Standard.

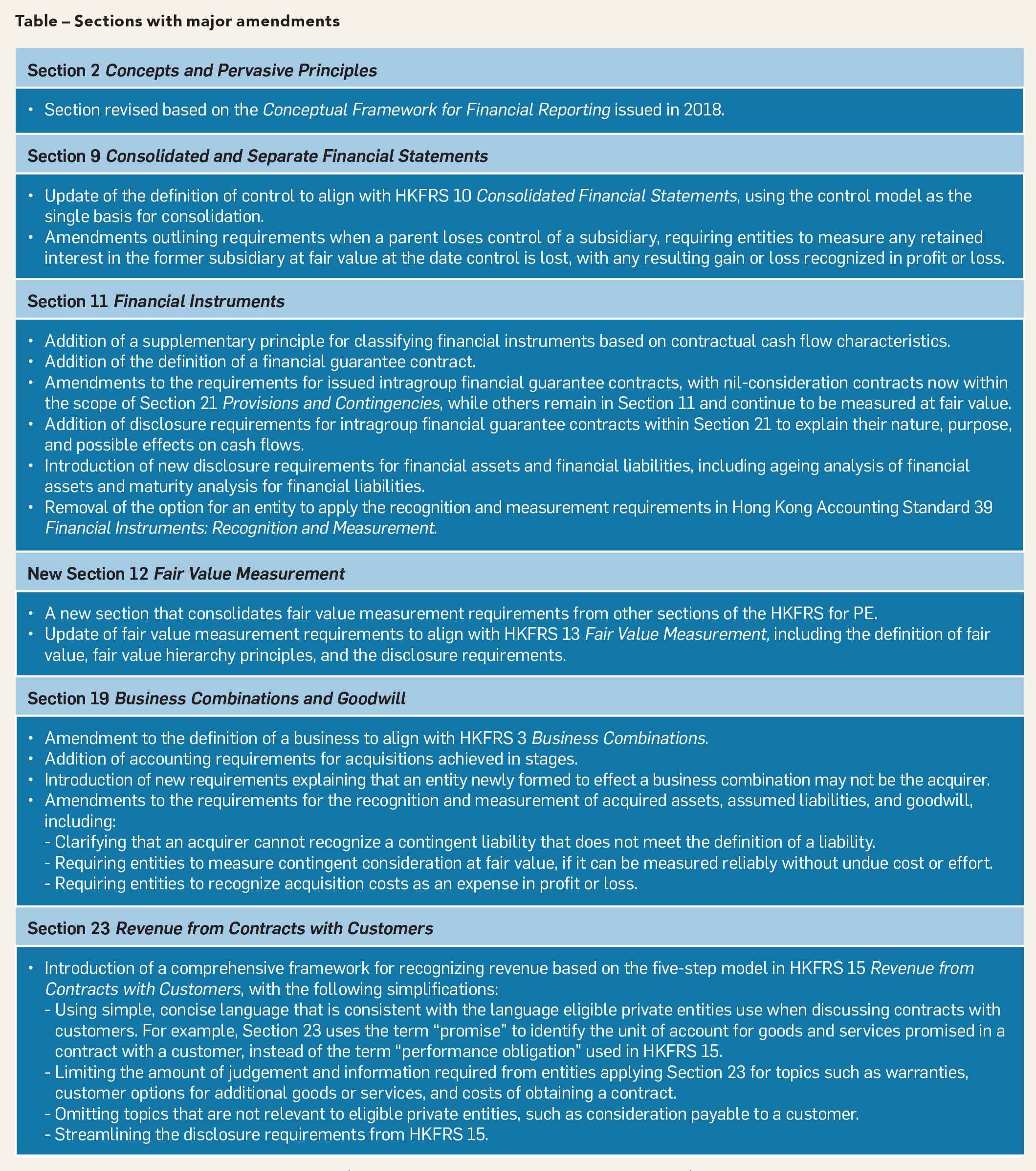

The revisions to the HKFRS for PE are extensive, covering nearly all sections of the standard. A list of the amendments can be found in the Introduction of the revised HKFRS for PE. The sections with major amendments, which are the focus of this article, are outlined below.

To understand how these major amendments impact local entities currently applying the extant HKFRS for PE, refer to Key impact of the 2025 revised HKFRS for PE on local entities issued by the Institute.

Although the revisions to the standard are extensive, there are a few areas where the current requirements have either been retained or not amended. These areas include:

Moreover, Section 20 Leases has not been amended to align with Hong Kong Financial Reporting Standard (HKFRS) 16 Leases in this revision. Any decisions on future alignment will be made only when more information about entities’ experience of applying HKFRS 16 is available.

The revised HKFRS for PE is effective for annual periods beginning on or after 1 January 2027, with early application permitted. Entities are required to apply the new and amended requirements in the revised HKFRS for PE retrospectively. However, some relief from retrospective application is available for entities applying certain amendments.

The amendments are comprehensive and will affect entities currently applying the extant HKFRS for PE. The impact ranges from changes in accounting policies and related accounting treatments to providing additional disclosures in the financial statements. Preparers should read the original text of the revised HKFRS for PE thoroughly to understand the amendments and assess how they will affect financial reporting based on the entity’s specific facts and circumstances.

For instance, the revised Section 23 Revenue from Contracts with Customers may result in some entities accounting differently for transactions with customers under the new five-step model. In addition, the new disclosure requirements in the revised Section 11 Financial Instruments, such as the aging analysis of financial assets and the maturity analysis for financial liabilities, require entities to collect additional information. Therefore, preparers should consider whether any changes to the systems, processes and controls are necessary in order to apply the new requirements.

The IASB has provided various support materials, including a Project Summary, Feedback Statement and Effects Analysis and podcasts, to assist entities with the implementation process. Additionally, the IASB is in the process of publishing updated educational modules, complemented by a webcast series, to provide further explanations and examples for applying the standard.

On the local front, the Institute plans to offer a webinar in the coming months to help entities understand the main features of the revised HKFRS for PE. Stay tuned for upcoming resource updates in the HKFRS for PE Information Centre and get in touch with the Institute’s Standard Setting Department through the Technical Enquiry system if you have any questions about implementing the revised HKFRS for PE.

This article was contributed by Anthony Wong and George Au, Associate Directors of the Institute’s Standard Setting Department.