As an accountant by training, and as a wealth advisor who has worked in traditional private banking and innovative WealthTech, I have learned one key truth in investing: While technology changes how we invest, successfully navigating the investing journey still depends on mastering a few core principles. Here are the three principles that separate disciplined investors from the rest.

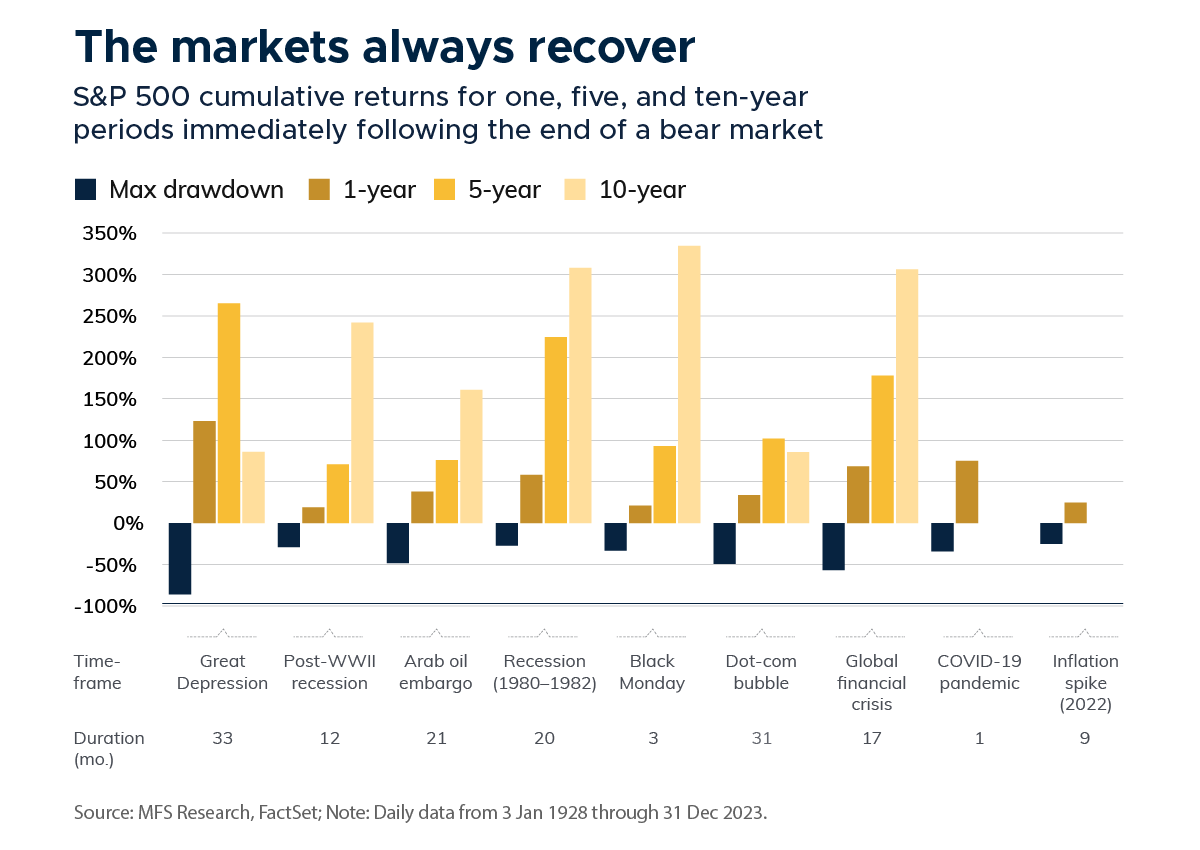

Master market cycles, not news headlines

The financial market has a recurring pattern of economic expansion, recession, and recovery. While volatility is an unavoidable part of investing, the most common mistake is reacting to sensationalist headlines that amplify short-term noise.

Through every major event - the dot-com bubble, the 2008 global financial crisis, the COVID-19 pandemic, the S&P 500 rebounded immediately in a year, with five-year cumulative returns ranging from 50% to over 200%. The story remains the same: markets ultimately reflect long-term economic fundamentals, and patient investors are rewarded.