In August 2023, the Institute’s Standard Setting Department responded to the International Sustainability Standards Board’s (ISSB) Request for Information (RFI) on its Consultation on Agenda Priorities after consultation with our local stakeholders. In June this year, the ISSB published the feedback statement on its agenda consultation, which sets out the ISSB’s responses to its feedback and 2024-2026 work plan.

Consistent with our stakeholder feedback, the ISSB decided:

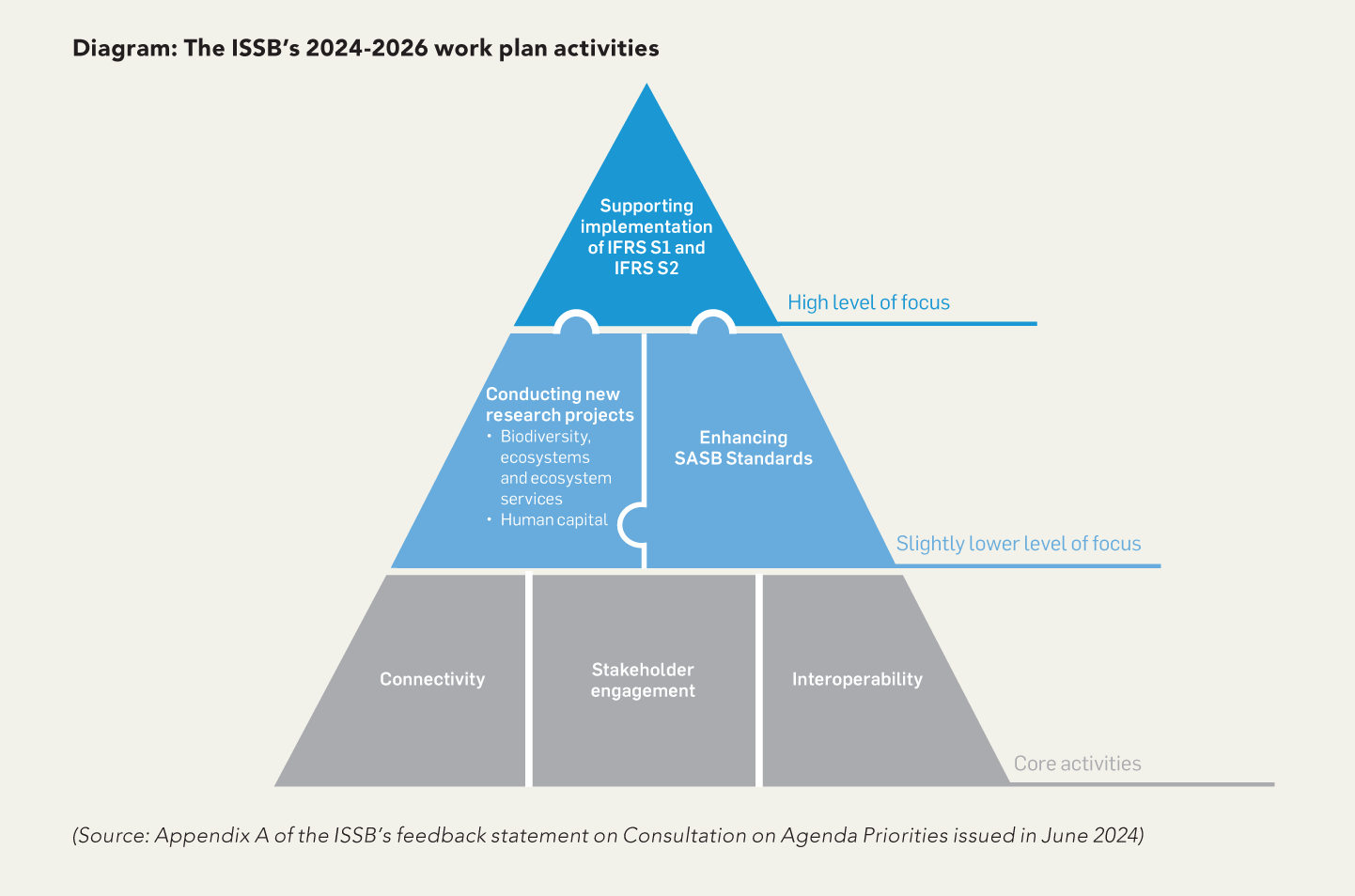

The diagram below illustrates the balance of the ISSB’s activities.

In addition, after considering stakeholder feedback and its own capacity, the ISSB has decided to add research projects on the risks and opportunities associated with the following topics to its work plan:

This aligns with our recommendation that the ISSB should undertake multiple projects and prioritize BEES as its primary focus.

The ISSB decided to place the highest priority on supporting the consistent and high-quality implementation of IFRS S1 and IFRS S2 by companies in jurisdictions around the world. A primary focus on this endeavour is crucial to establish a global baseline of sustainability-related financial disclosures.

The ISSB acknowledges the importance of maintaining and enhancing the SASB Standards to support the implementation of IFRS S1 and IFRS S2, as well as to ensure their ongoing relevance and suitability for a global audience. The ISSB has decided to allocate a high but slightly lower level of focus to enhancing the SASB Standards in comparison to supporting the implementation of IFRS S1 and IFRS S2.

The ISSB recognizes the significance of beginning new research projects to enhance the global baseline of sustainability-related financial disclosures. It also acknowledges the feedback, particularly from investors, emphasizing that the successful implementation of IFRS S1 and IFRS S2 is crucial in establishing this global baseline and could take precedence over commencing new research projects. However, IFRS S1 requires companies to report on matters beyond climate with reference to materials such as the SASB Standards. Therefore, conducting new research on sustainability-related matters may contribute to the effective implementation of IFRS S1. In addition, researching industry-specific considerations can inform improvements to the SASB Standards. Accordingly, the ISSB has decided to assign a high but slightly lower level of focus to beginning new research projects compared to supporting the implementation of IFRS S1 and IFRS S2.

Given the capacity limitations of the ISSB, it is unlikely that they will be able to deliver ISSB Standards or significantly advance all proposed projects within the two-year work plan outlined in the RFI. Each project requires extensive research and analysis to determine the necessity and feasibility of standard-setting.

The ISSB’s capacity is constrained because a portion of it is dedicated to supporting the implementation of IFRS S1 and IFRS S2, as well as enhancing the SASB Standards. The ISSB has also taken into account other capacity-related factors, including their lack of prior comparable experience to estimate capacity requirements, the impact of project scope on the speed of progress, and the need to allocate capacity for emergent issues.

Moreover, recognizing the vital importance of engaging with stakeholders in the ISSB’s work, the capacity of stakeholders to actively participate in projects holds significant value. Therefore, by considering these capacity constraints and applying its criteria for assessing the priority of proposed projects, the ISSB has made the decision to undertake research projects that specifically focus on the risks and opportunities associated with:

Biodiversity, ecosystems and ecosystem services

Each part of BEES is inherently interconnected. Biodiversity serves as a fundamental attribute of natural systems, serving as an indicator for the functionality, productivity, and resilience of ecosystems that provide essential ecosystem services vital for life on Earth. Numerous economic activities are reliant on or impact BEES in various ways. Consequently, endeavours aimed at preserving, conserving, and restoring BEES can contribute to risk management and create opportunities for companies. It is reasonable to anticipate that these risks and opportunities can significantly impact a company’s prospects, as outlined in IFRS S1, and may generate material information that is relevant to investors.

Human capital

Human capital encompasses the individuals comprising a company’s internal workforce as well as workers involved in its value chain. In line with the Integrated Reporting Framework, human capital also refers to the competencies, capabilities, experiences, and motivations of the workforce and workers, fostering innovation. How a company manages and invests in its human capital directly impacts its capacity to generate long-term value. Human capital management includes various aspects such as workforce composition, stability, diversity and inclusion, training and development, health, safety, wellbeing, and compensation. While human capital management is relevant to all companies due to their employee base, the ways in which human capital influences value can differ. Research suggests that, depending on a company’s business model, a diverse workforce can enhance talent attraction and retention, facilitate effective product and service design, marketing, and delivery, strengthen community relations, drive innovation, and identify risks.

This article was contributed by Anthony Wong, Associate Director of the Institute’s Standard Setting Department.