The Inland Revenue (Amendment) (No. 3) Bill 2018 (the bill), passed by the Legislative Council on 24 October, implements measures proposed by the Chief Executive in her 2017 Policy Address to provide for enhanced tax deductions for qualifying expenditures on qualifying research and development (R&D) activities to encourage more private sector R&D activities in Hong Kong. During its passage through the Bills Committee of the Legislative Council, only one major Committee Stage Amendment was proposed by the Secretary for Innovation and Technology, to allow a grace period for taxpayers to enjoy the tax deduction in respect of payments made to a local institution or local research institution which subsequently qualifies as a designated local research institution within six months after the date of payment. The new regime will take retrospective effect and apply to R&D expenditures incurred on or after 1 April 2018. In this article, we will discuss the key elements of the bill, practical issues regarding the regime, and some additional measures that may be considered by the government in order to develop Hong Kong into a true R&D hub and increase the city’s competitiveness.

Two types of R&D expenditures as defined in the bill

The deduction for R&D expenditures is currently governed by section 16B of the Inland Revenue Ordinance (IRO). The bill proposes to revamp the current R&D deduction regime by introducing a new Schedule 45 to the IRO that sets out two deduction criteria under section 16B: Type A expenditure which qualifies for 100 percent normal tax deduction (as currently provided); and Type B expenditure which qualifies for 300 percent deduction for the first HK$2 million and 200 percent for the remaining amount, without a cap.

Meaning of R&D activity and qualifying R&D activity

Pursuant to Part 1 of Schedule 45, the definition of an R&D activity is unchanged from the existing definition in section 16B(4)(a) of the IRO, namely:

(a) An activity in the fields of natural or applied science to extend knowledge;

(b) A systematic, investigative or experimental activity carried on for the purposes of any feasibility study or in relation to any market, business or management research;

(c) An original and planned investigation carried on with the prospect of gaining new scientific or technical knowledge and understanding; or

(d) The application of research findings or other knowledge to a plan or design for producing or introducing new or substantially improved materials, devices, products, processes, systems or services before they are commercially produced or used.

Qualifying R&D activities only cover activities as described under (a), (c) or (d) above and which are wholly undertaken and carried on in Hong Kong. Additionally, a qualifying R&D activity does not include the following:

- Any efficiency survey, feasibility study, management study, market research or sales promotion;

- The application of any publicly available research findings or other knowledge to a plan or design, with an anticipated outcome and without any scientific or technological uncertainty;

- An activity that does not seek to directly contribute to achieving an advance in science or technology by resolving scientific or technological uncertainty; or

- Any work to develop the non-scientific or non-technological aspect of a new or substantially improved material, device, product, process, system or service.

Definitions of Type A and Type B expenditures

Type B expenditures eligible for enhanced deductions refer to the following expenditures incurred by a taxpayer in relation to his trade, profession or business:

- Payments made to designated local research institutions for conducting out-sourced qualifying R&D activities; or

- Expenditures such as salaries, wages and contributions to retirement or provident fund schemes paid in respect of employees (excluding directors) directly and actively engaged in qualifying R&D activities, and consumable items used directly in qualifying R&D activities.

Type A expenditure is defined as R&D expenditure on an R&D activity or a qualifying R&D activity other than Type B expenditure. Capital expenditure on plant or machinery used in an R&D activity, for instance, falls within Type A expenditure eligible for a 100 percent tax deduction.

Designated local research institutions

Under the current section 16B, R&D payments made to “approved research institutes” qualify for 100 percent deduction. At the moment, there are only five approved research institutes, all of which are public institutions. Under the new regime, in order to boost R&D activities in the private sector, it is expected that more institutions, including private ones, will be granted the designated local research institution status.

Under the bill, the Commissioner of Innovation and Technology (CIT) is empowered to approve an entity as a designated local research institution. In determining an application, the CIT will consider factors such as whether or not the institution possesses expertise in providing R&D services in one or more specified fields of science or technology, sufficient qualified and experienced R&D employees, equipment and facilities, sound project management experience, and appropriate track records. Details of the eligibility criteria are expected to be announced soon.

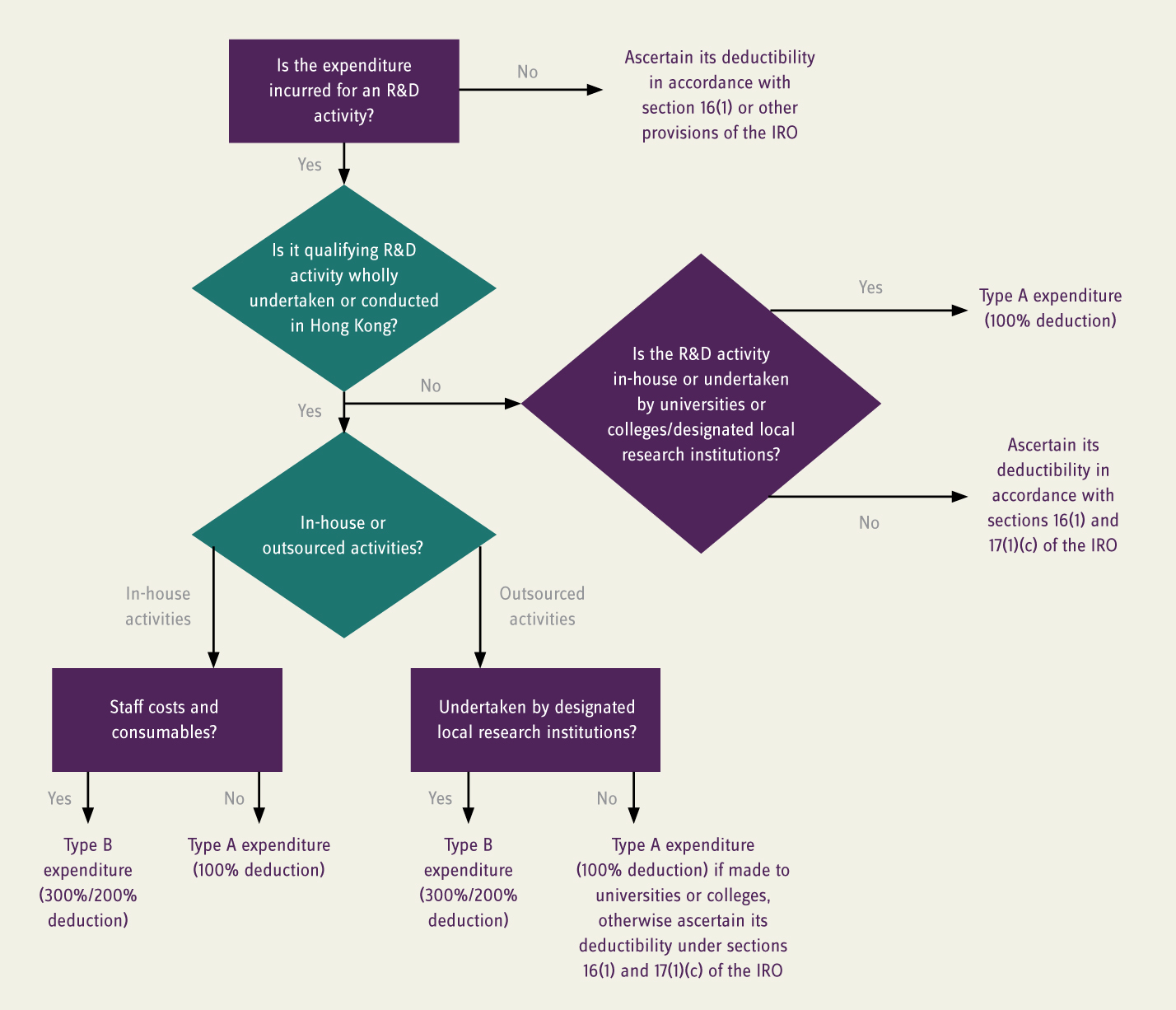

Classification of R&D expenditures

The decision tree below illustrates the classification of R&D expenditures (excluding capital expenditures on land or buildings and acquiring rights generated from an R&D activity) incurred by a taxpayer and the relevant tax treatments under the new regime.

Deduction safeguard measures proposed in the bill

Part 2 of Schedule 45 includes certain safeguards to prevent the abuse of the R&D deduction regime by a taxpayer. No deduction is available under section 16B in the following circumstances:

- Any rights generated from the R&D activities are not, or will not be, fully vested in the taxpayer;

- The R&D activities are undertaken by the taxpayer for another person;

- The expenditure is, or will be, met directly or indirectly by grants or subsidies by a government, a public or local authority or a person other than the taxpayer, whether in Hong Kong or elsewhere; or

- The expenditure is incurred under an arrangement the main purpose, or one of the main purposes, of which is to obtain a deduction or a greater deduction to which the taxpayer would not otherwise be entitled under section 16B.

Co-ownership of intellectual property (IP), which is commonly the case under a cost sharing arrangement, is acceptable as being fully vested in the taxpayer, as “rights” is defined to include a share or an interest in rights.

Taxability of the proceeds of sales of rights/plant or machinery

Part 3 of Schedule 45 stipulates that proceeds from the sale of any rights generated from the relevant R&D activities, or any proceeds from the sale of plant or machinery or insurance moneys or other compensation received where the plant or machinery is destroyed, capped at the amount of the total deductions allowed under section 16B, will be considered as taxable receipts.

Supporting documentation and the involvement of Innovation and Technology Commission in the R&D deduction claims

In order to support the R&D deduction claim, taxpayers must demonstrate that the activities undertaken will lead to an advance in science or technology by resolving uncertainty in the fields of the trade, profession or business engaged by taxpayers, with consideration of the state of knowledge and technology at project commencement.

Taxpayers should be prepared to provide documentary records of the R&D activities conducted to substantiate their deduction claims.

Before project commencement, project plans and budget papers which clearly define the objectives and the exact scientific or technological uncertainties to be overcome should be in place.

During the project, taxpayers should maintain laboratory notes, internal progress reports and other relevant documents which discuss any major challenges encountered and how the results, if any, are being crystallized and protected. Nevertheless, qualifying R&D activities which ultimately fail to achieve the intended results should not prevent the underlying expenditures from enjoying the enhanced R&D deduction.

More practical guidance and examples on the types of activities accepted as qualifying R&D activities and details of documentary evidence required supporting R&D deduction claims are expected to be provided in the forthcoming Departmental Interpretation and Practice Notes to be issued by the Inland Revenue Department (IRD). The IRD also welcomes advance ruling applications by taxpayers.

It is envisaged that the IRD will adopt a risk-based approach to carry out sample examination of R&D deduction claims made by taxpayers. In view of the potentially extensive documentation requirements, the organization’s finance team should ensure effective communication with the R&D personnel such that the relevant supporting documentation is properly maintained and can be retrieved on a timely basis. In particular, in determining whether expenditures incurred for R&D projects qualify for normal or enhanced R&D deduction, accounting classifications of the expenditures may not be conclusive, and input from the R&D team members may be necessary. A close and regular dialogue between the R&D and finance teams throughout the entire process is of utmost importance.

Under the bill, the Commissioner of Inland Revenue (CIR) is empowered to seek advice from the CIT when processing section 16B claims or advance ruling applications. The CIR may disclose to the CIT any necessary details for the consultation.

While it is understandable that expert advice from the CIT may be necessary in assessing claims or resolving disputes, the business sector would hope that the additional consultation would not lead to significant delay in processing claims and approving the designated local research institution status. The IRD and Innovation and Technology Commission should make concerted efforts to provide an administrative friendly environment for taxpayers to enjoy the new incentive in order to foster the growth of R&D activities in Hong Kong.

New deeming provision on trading receipts

The bill also introduces a new deeming provision under section 15 of the IRO to include, as taxable trading receipts, sums received or accrued (i) for the use, or the right to the use, outside Hong Kong of any IP or know-how generated from any R&D activities for which deductions are allowable under section 16B of the IRO; or (ii) for imparting or undertaking to impart knowledge directly or indirectly connected with the use outside Hong Kong of any such property or know-how.

The introduction of deeming provisions, especially along with tax incentive regimes, appears to have become the norm in Hong Kong in recent years. While the inclusion of measures to avoid abuse is understandable, a fair balance needs to be struck as such deeming provisions are, arguably unnecessarily, undermining the fundamental territorial basis of taxation of Hong Kong. Moreover, the broadening of the tax base through these deeming provisions further reduces the attractiveness of Hong Kong as a place to hold and exploit IP.

Further measures to encourage private sector R&D activities in Hong Kong

Whilst the introduction of the enhanced R&D deduction regime is a good move, the deductions are still relatively restricted. For instance, R&D payments made to non-Hong Kong persons or Hong Kong persons that are not designated local research institutions (other than colleges or universities) are non-deductible under section 16B. In comparison, Mainland China has recently relaxed its R&D super-deduction regime to cover R&D payments made to overseas parties as long as the relevant IP rights are owned in Mainland China. Given the current lack of sufficient R&D talents in Hong Kong, the government may consider further enhancing the regime to relax the rules on expenditures incurred overseas, while Hong Kong develops local expertise. The government may also consider expanding the scope of in-house R&D expenditure eligible for the enhanced deduction to cover other R&D related expenditures, such as overhead costs, costs of independent contractors and capital expenditure on plant or machinery. To further improve the overall R&D atmosphere in Hong Kong, the government may consider offering incentives to qualified R&D talents who move to Hong Kong.

In order to further build up a sustainable ecosystem that attracts capital for R&D activities in Hong Kong as well as encouraging the owning of IP rights in Hong Kong, the government may wish to revisit the taxation rules concerning IP. The current restrictive deduction rules on IP acquisition costs coupled with stringent taxing rules and practice on IP related income and lack of unilateral double tax relief for foreign tax paid in a non-treaty jurisdiction may give rise to an exceptionally high effective tax rate for an IP-owning company in Hong Kong in certain circumstances. Further effort is needed for Hong Kong to gain its position as one of the competitive R&D and IP hubs in the Asia Pacific region.

In her maiden Policy Address, the Chief Executive set the goal of doubling R&D expenditure to 1.5 percent of the GDP in Hong Kong within the current government’s five-year tenure. While the proposed enhanced R&D deduction is in the right direction to encourage the private sector to invest more in R&D, the government should keep up the momentum in formulating and rolling out more tax and non-tax measures in promoting R&D spending in Hong Kong. The bill is only the first chapter of this journey.

Gwenda Ho is Tax Partner and Ricky Chow is Tax Senior Manager of PwC Hong Kong.