Hong Kong is making significant strides to step up innovation and intellectual property (IP) development. A pivotal step is the introduction of the patent box regime, a tax incentive designed to encourage the development and commercialization of IP within Hong Kong.

Legislative background

The patent box regime was officially enacted through the Inland Revenue (Amendment) (Tax Concessions for Intellectual Property Income) Ordinance 2024 (the Amendment Ordinance), gazetted on 5 July 2024 which is applicable to the year of assessment 2023/24 onwards. It introduces a 5 percent concessionary tax rate for Hong Kong-sourced taxable (i.e. non-capital) profits derived from the use or sale of eligible IP, subject to certain conditions, in particular an apportionment based on the research and development (R&D) fraction.

Eligibility criteria

The tax incentive is available to taxpayers deriving eligible income from eligible IP, including economic owners.

Eligible IP includes the following categories of IP generated from an R&D activity: (1) a patent granted or applied for in Hong Kong or overseas, (2) a plant variety right granted or an application filed under Hong Kong law, and (3) copyrighted software.

For short-term patents, a post-grant substantive examination request must be filed with the Patents Registry in Hong Kong within a specified period. Concerning patents or plant variety rights granted outside Hong Kong, or applications for such rights filed outside Hong Kong, if the filing date is on or after 24 months following 5 July 2024, there must be a corresponding local application or grant in Hong Kong to meet the local registration requirement.

For copyrighted software, although a registration is generally not required under Hong Kong or foreign laws, the copyright subsisting in the software must fall within the scope of legal protection. Further guidance and illustrative examples are expected to clarify this requirement.

Given the widespread use of software across various industries, it would be helpful if the forthcoming guidance were to explain what information or evidence taxpayers need to provide to demonstrate that the software qualifies. Such clarification is crucial, as the relevant copyright or protection is usually acquired automatically when an original work is created.

Types of income covered

To qualify for the patent box tax incentive, income must be Hong Kong-sourced and fall into one of the following categories of eligible IP income:

- Income from use or right to use eligible IP;

- Income from the sale of eligible IP;

- Portion of income from sale of a product or service attributable to eligible IP, determined on a just and reasonable basis; and

- Insurance, damages, or compensation derived in relation to eligible IP.

With the broad range of eligible IP income, the application of the patent box regime could be more extensive than anticipated. In addition to the businesses typically associated with IP, such as those in the technology and pharmaceutical industries, this tax incentive could potentially extend to, e.g. the financial services sector in relation to its evolving fintech businesses.

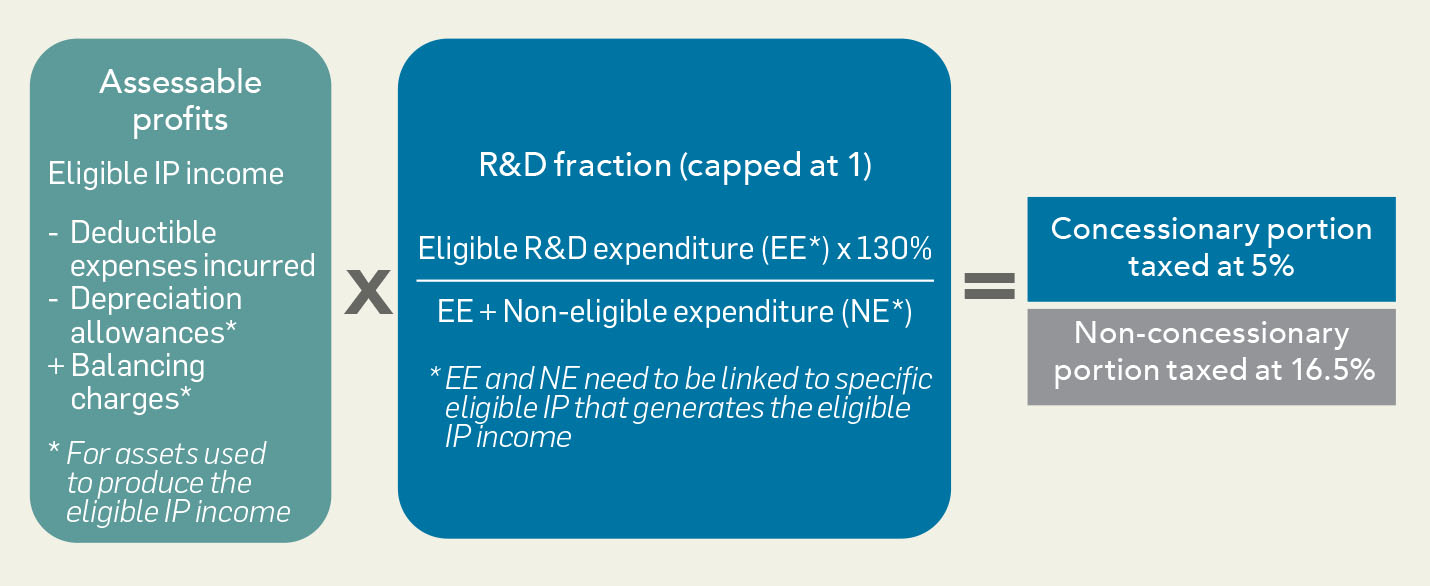

The R&D fraction and concessionary portion of assessable profits

The patent box tax incentive adopts the OECD’s nexus approach, requiring taxpayers to track and link expenditure and IP income to specific IP assets. The portion of assessable profits eligible for the 5 percent concessionary tax rate is calculated based on the R&D fraction shown below.

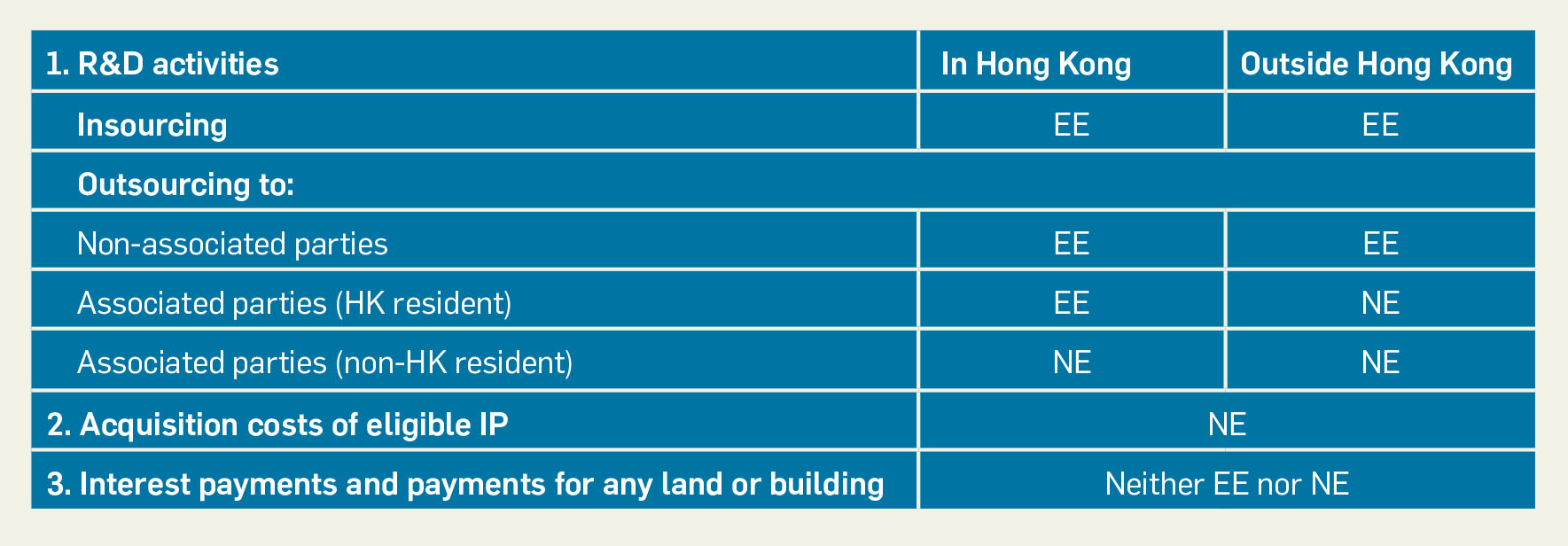

The types of eligible R&D expenditure (EE) and non-eligible expenditure (NE) are outlined below.

Increased R&D activities within Hong Kong would generally result in a higher R&D fraction, allowing a larger portion of assessable profits benefiting from the concessionary tax rate. This approach incentivizes businesses conducting R&D activities locally.

A tax loss incurred by a taxpayer in relation to income benefiting from the patent box tax incentive can be offset against the taxpayer’s other assessable profits, subject to tax rate differential adjustment.

Compliance and administration

A taxpayer has to make an irrevocable election in the relevant profits tax return and complete a corresponding Form IR1482, and notify the Inland Revenue Department if a granted eligible IP is subsequently revoked or cancelled, or if a patent application is declined or withdrawn. Businesses must also retain detailed transaction and business records for seven years after the completion of relevant transactions, or seven years after the election, whichever is later.

Competitive edge

Both Hong Kong’s patent box regime and Singapore’s IP Development Incentive (IDI) aim to foster innovation and attract IP development with different features and advantages.

Tax concession

Both Hong Kong and Singapore adhere to the OECD’s nexus approach ensuring the tax benefits are aligned with substantial R&D activities within the jurisdiction. While the calculation of the concessionary portion of assessable profits eligible for the preferential tax rate is the same, the preferential tax rates are however different:

- Hong Kong’s patent box tax incentive applies a flat 5 percent tax rate on the concessionary portion of assessable profits.

- Singapore’s IDI offers a tiered tax rate of either 5 percent, 10 percent or 15 percent, where the lower rate applies to businesses that meet a higher annual business spending requirement. In addition, during the extended period (not more than 10 years for each extension, see below), the concessionary tax rate will increase by at least 0.5 percent at regular intervals.

Economic substance requirements

IDI includes quantitative economic requirements regarding (1) the number of skilled employees in Singapore and (2) annual business expenditure, and qualitative assessments of the underlying project(s). In contrast, Hong Kong does not impose additional economic substance requirements beyond the nexus approach.

Eligible industries and IP

Hong Kong’s regime does not impose industry-specific restrictions, making it accessible, in theory, to a wide range of businesses. Singapore’s IDI, however, excludes certain industries, such as financial institutions, shipping enterprises, and tobacco manufacturers.

Both regimes cover similar types of eligible IP. However, Hong Kong mandates local registration for patents and plant variety rights granted outside the jurisdiction after a “24-month grace period”, while Singapore does not impose a local registration requirement for qualifying IP.

Eligible income

Hong Kong’s regime includes a broad spectrum of income types, while Singapore’s IDI primarily focuses on royalties and other income from the commercial exploitation of qualifying IP. This broader scope in Hong Kong allows for greater flexibility in the types of income that can benefit from the concessionary tax rate.

Pre-approval requirements and subsequent administration burden

Hong Kong’s regime does not require formal application or pre-approval, reducing administrative burdens. Singapore’s IDI requires a formal application process and annual progress updates.

Other considerations

Hong Kong’s patent box tax incentive requires businesses to track income and R&D expenditure for each eligible IP, while Singapore allows grouping of IP into families, providing more flexibility.

From a policy standpoint, Hong Kong’s regime offers indefinite incentive periods without a sunset clause as long as the concessionary conditions are met. In contrast, the incentive period for Singapore’s IDI is limited to 10 years, with possible extensions not exceeding 10 years each time, with incremental economic commitments. Additionally, there is a sunset clause with the IDI set to end on 31 December 2028. These policy differences significantly impact strategic business planning, with Hong Kong providing more stability for long-term investments.

The expected enactment of corporate inward re-domiciliation laws in Hong Kong will allow the “transfer” of IP holding vehicles to Hong Kong, bringing Hong Kong and Singapore on a par in this regard.

Conclusion and future outlook

The introduction of Hong Kong’s patent box regime is a crucial step in its ambition to lead in innovation and IP development. By offering a 5 percent concessionary tax rate on eligible IP income, the regime encourages local R&D and IP commercialization, aligning with global standards and enhancing Hong Kong’s competitive position against other financial hubs like Singapore. Possible (enhanced) R&D deductions would further incentivize IP-related businesses to base and grow in Hong Kong.

This article is co-authored by Eugene Yeung, Partner of KPMG China and Chair of the Institute’s Taxation Faculty Executive Committee, and Edmond Ma, Tax Manager of KPMG China.