Background of the amendments

In May 2024, the International Accounting Standards Board (IASB) issued Amendments to the Classification and Measurement of Financial Instruments, which amended International Financial Reporting Standard (IFRS) 9 Financial Instruments and IFRS 7 Financial Instruments: Disclosures, to address the matters identified during the post-implementation review (PIR) of the classification and measurement of IFRS 9 and clarify stakeholders’ concerns and emerging issues. The Hong Kong Institute of CPAs issued the equivalent Amendments to Hong Kong Financial Reporting Standard (HKFRS) 9 Financial Instruments and HKFRS 7 Financial Instruments: Disclosures in August 2024. The key areas of the amendments include:

(i) Clarifying the date on which a financial asset or financial liability is derecognized;

(ii) Introducing an accounting policy option to derecognize financial liabilities that are settled through an electronic payment system before settlement date if specified criteria are met;

(iii) Clarifying the classification of financial assets with environmental, social and corporate governance (ESG) and other similar features;

(iv) Clarifying the requirements for classifying financial assets with non-recourse features and contractually linked instruments; and

(v) Additional disclosure requirements regarding investments in equity instruments designated at fair value through other comprehensive income (FVTOCI) and financial instruments with contingent features, for example, features tied to ESG-linked targets.

Among these amendments, we consider those related to the initial recognition or derecognition of financial assets and liabilities (i.e. (i) and (ii) above) and the classification of financial assets with ESG-linked features, as well as the related disclosures (i.e. (iii) and (v)) to be particularly relevant for the majority of reporting entities in Hong Kong. Accordingly, this article focuses on highlighting these requirements and their implications. It does not cover the amendments related to non-recourse features and contractually linked instruments.

Please note that the discussions regarding the implications of the key amendments below are not exhaustive. Entities should read the full amendments and conduct their own assessments based on their specific facts and circumstances.

Highlights of key amendments and their relevant implications

- Initial recognition or derecognition of financial assets and liabilities

Date of initial recognition or derecognition of financial assets and liabilities – general principles

The amendments clarify that financial assets or financial liabilities are recognized when the entity becomes a party to the contractual provisions of the instrument. Regarding derecognition, financial assets are derecognized when the entity’s rights to the contractual cash flows expire or are transferred. In the case of financial liabilities, the amendments clarify that a financial liability is derecognized on the “settlement date”, i.e. the date on which the financial liability is extinguished because the related obligation specified in the contract is discharged, cancelled, expires or the liability otherwise qualifies for derecognition.

Implications and relevant considerations

Unless using an electronic payment system that meets the specified criteria in HKFRS 9.B3.3.8 (refer to “Derecognition of a financial liability through electronic transfer” below), entities cannot derecognize a financial asset or financial liability until the amount has cleared in the receiving entity’s bank account. These requirements apply to payments made via cheque, debit card or credit card and other electronic transfers that do not satisfy the conditions in HKFRS 9.B3.3.8.

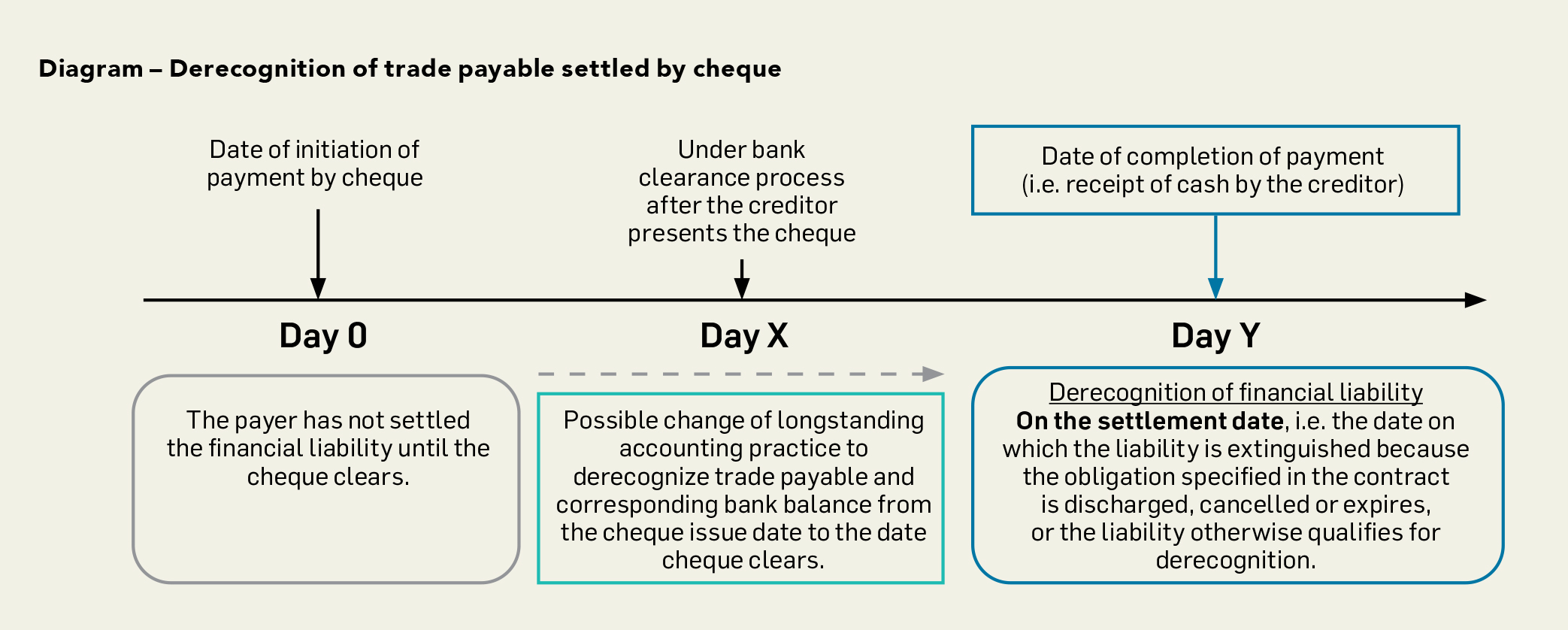

In Hong Kong, it is common for companies to derecognize their financial liabilities upon the issuance of cheques to their creditors. At each month-end, they perform bank reconciliation procedures to reconcile any differences in the closing balance between the bank ledger and bank statements (e.g. cheques not yet cleared by the bank). The amendments could change this current practice by clarifying that entities can derecognize their financial liabilities only when cheques are cleared by the bank, instead of when they are issued, as illustrated in the diagram below.

Under the amendments, the debtor should derecognize trade payable on Day Y when the creditor receives the cash, as opposed to Day 0 when the debtor issues the cheque. Similarly, a creditor derecognizes a trade receivable upon receiving cash from the debtor after the cheque has been cleared by the bank.

As illustrated in the diagram, entities whose current financial reporting processes do not align with the clarifications provided in the amendments might be affected. Therefore, entities should revisit their processes and assess whether the accounting policy for derecognition of financial assets and financial liabilities conforms to the amendments.

Derecognition of a financial liability through electronic transfer

The amendments introduce an accounting policy option that allows an entity to deem a financial liability (or part of it) to be settled in cash using an electronic payment system as discharged before the settlement date if the conditions specified in HKFRS 9.B3.3.8 are met. This enables the entity to derecognize the financial liability before the settlement date. This option does not apply to other means of settling financial liabilities, such as payments by cheque, debit card or credit card. Once an entity elects this accounting policy option, it is required to apply that accounting policy to all settlements made through the same electronic payment system. However, the option can be applied to electronic payments on a system-by-system basis.

Implications and relevant considerations

The amendments are not expected to have a significant impact on entities operating in Hong Kong and Mainland China where electronic payment systems generally operate on a real-time basis.

However, it is important to note that the amendments apply to specific scenarios involving payments made through an electronic payment system for financial liabilities. For entities intending to apply the accounting policy option permitted by the amendments, additional work will be required to analyze the contractual and legal requirements for each electronic payment system in their jurisdictions to determine whether the specified conditions are met. This analysis could be complex, particularly in cases of cross-border payments. Furthermore, entities’ financial reporting processes might be affected, for example, some entities that previously derecognized financial liabilities only upon cash receipts will need to adjust their practices if the accounting policy option is adopted.

- Classification of financial assets – contractual terms that are consistent with a basic lending arrangement

The PIR of IFRS 9 discussed the challenges raised by stakeholders regarding the classification of financial assets with contingent features whose cash flows are linked to ESG targets. Questions have been raised as to whether the contractual cash flows from these financial assets are solely payments of principal and interest on the principal amount outstanding (SPPI) under IFRS 9. In response to the stakeholders’ feedback, the IASB amended IFRS 9 to provide guidance on how an entity assesses whether contractual cash flows of a financial asset with contingent features are consistent with a basic lending arrangement, specifically, whether:

- The contractual cash flows that could arise before and after the change in contractual cash flows would meet the SPPI test.

- The nature of contingent event relates directly to, and the contractual cash flows change in the same direction as, changes in basic lending risks and costs.

- The SPPI test may still be met when the nature of contingent event does not relate directly to changes in basic lending risks and costs.

To illustrate the application of the requirements, the amendments also add examples of financial assets with contingent features that have, or do not have, contractual cash flows that are SPPI.

Implications and relevant considerations

The amendments provide additional application guidance for all financial assets whose contractual cash flows could change as a result of contingent events. Therefore, entities should reassess whether their financial assets with contingent features are impacted by the amendments. Judgement may be needed in assessing whether financial assets containing contingent features satisfy the SPPI test under the amendments, e.g. what is considered as “significantly different” in applying the new requirements of HKFRS 9.B.4.1.10A.

In cases where there is a change in the measurement category of existing financial assets as a result of applying the amendments, entities should provide the relevant disclosures according to the transition provisions in the amendments.

- Disclosures

Disclosures – investments in equity instruments designated at FVTOCI

The amendments require the following additional disclosures for each class of FVTOCI investments:

- The change in fair value in other comprehensive income during the period, showing separately the amounts related to investments derecognized in the period, and those held at the end of the reporting period; and

- The aggregate fair value of investments (as opposed to fair value of each such investment before the amendments) at the end of the reporting period.

The amendments also require disclosure of any transfers of the cumulative gains and losses within equity during the reporting period related to the FVTOCI investments derecognized in that reporting period.

In addition, the amendments provide an example in the Implementation Guidance to HKFRS 7 to illustrate the application of the above new disclosure requirements.

Implications and relevant considerations

The grouping of investments into classes should be performed based on the requirements of HKFRS 7.6. The applicability of the new disclosure regarding the transfers of cumulative gains or losses within equity depends on the entities’ existing accounting policy on whether to transfer these cumulative gains or losses.

Disclosures – contractual terms that could change the timing or amount of contractual cash flows on the occurrence (or non-occurrence) of a contingent event

The amendments introduce new disclosure requirements to enable users of financial statements to understand the effect of contractual terms that could change the timing or amount of contractual cash flows based on the occurrence (or non-occurrence) of a contingent event that does not relate directly to changes in basic lending risks and costs. These new disclosures include:

- A qualitative description of the nature of the contingent event;

- Quantitative information about the possible changes to contractual cash flows that could result from those contractual terms; and

- The gross carrying amount of financial assets and the amortized cost of financial liabilities subject to those contractual terms.

The above disclosure requirements apply to each class of financial assets measured at amortized cost or FVTOCI and each class of financial liabilities measured at amortized cost.

Implications and relevant considerations

The new disclosures are applicable to both financial assets and financial liabilities whose cash flows would change due to a contingent event, and not only financial assets whose classification requirements have been amended. They are not required for financial instruments measured at fair value through profit or loss, as the changes in fair value are considered to provide sufficient information to enable users to assess the future cash flows of those instruments.

While entities should group investments into classes based on the requirements of HKFRS 7.6, judgement may be necessary when determining the appropriate level of aggregation or disaggregation of information for disclosures. In addition, entities may need to exercise judgement in determining the nature and extent of qualitative and quantitative disclosures required by the amendments, taking into account the complexity of the instruments and materiality.

Effective date and transition

The amendments will become effective for annual reporting periods beginning on or after 1 January 2026. Earlier application of either all the amendments at the same time or only the amendments related to the classification of financial assets and the related disclosures is permitted. An entity shall apply the amendments retrospectively. Restatement of comparative information is not required, and is only permitted to do so without the use of hindsight.

This article was contributed by Carrie Lau and Kennis Lee, Associate Directors of the Institute’s Standard Setting Department. Visit our “What’s new” webpage for our latest publications, and follow us on LinkedIn for upcoming activities.