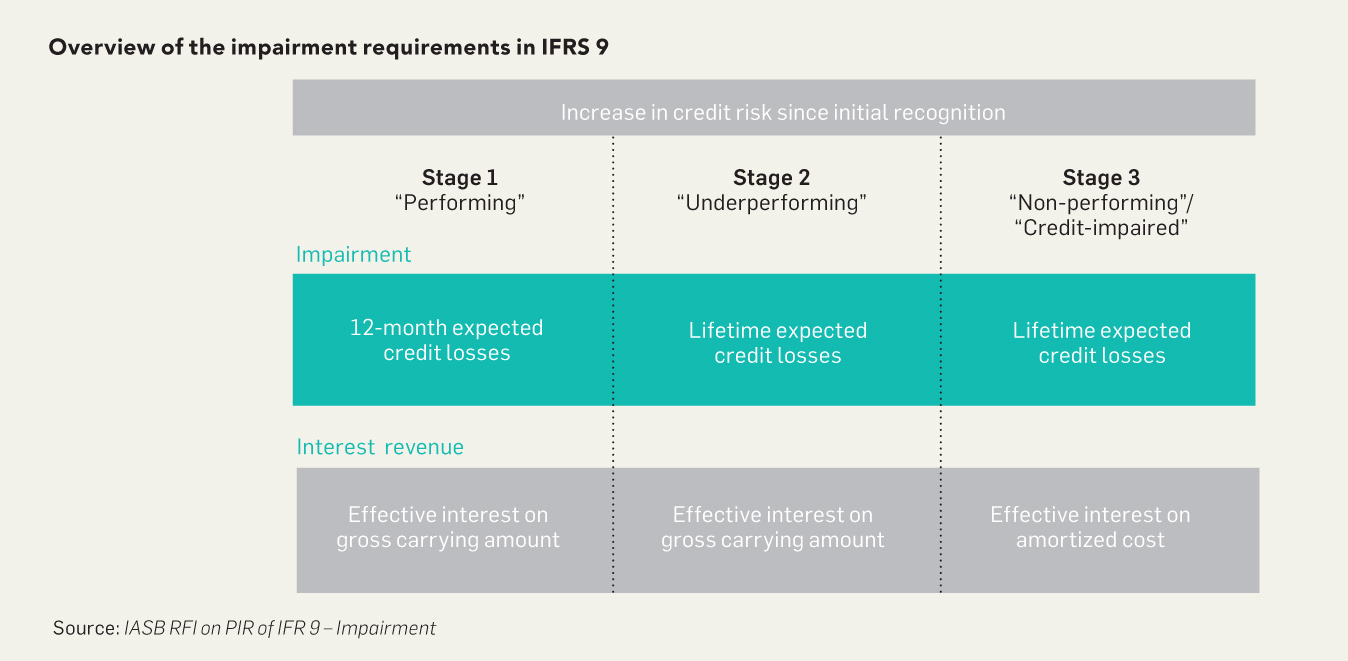

International Financial Reporting Standard (IFRS) 9 Financial Instruments sets out the requirements for recognition of expected credit losses (ECL) for all financial instruments that are subject to impairment accounting. The impairment requirements in IFRS 9 were developed in response to the global financial crisis and stakeholders’ calls for more timely recognition of loan losses and a forward-looking impairment model. The ECL model in IFRS 9 replaced the previous “incurred credit loss” model in International Accounting Standard (IAS) 39 Financial Instruments: Recognition and Measurement, which only allowed credit losses to be recognized when a loss event occurred. Under the ECL model, companies are required to recognize and update ECL throughout the life of a financial asset, factoring in the losses they expect based on relevant available information.

The International Accounting Standards Board (IASB) is currently undertaking a Post-implementation Review (PIR) of the impairment requirements in IFRS 9. As part of this review, the IASB has published a Request for Information (RFI) to seek feedback from stakeholders on specific areas of the impairment requirements and the related disclosures. In September, the Institute’s Standard Setting Department responded to the RFI. This article highlights our primary comments outlined in our submission. The full response is available on our website.

Overall, we consider that the use of the ECL model in IFRS 9 results in more timely recognition of credit losses and provides better information about an entity’s ECL as compared to the incurred loss model in IAS 39. Nevertheless, we have identified the following application issues that warrant the IASB’s further consideration.

Meaning of “credit loss”

In our submission to the IFRS Interpretations Committee tentative agenda decision Lessor Forgiveness of Lease Payments (IFRS 9 and IFRS 16), we expressed concerns over the unclear meaning of “credit loss” for the purpose of ECL assessment. On the one hand, Appendix A of IFRS 9 defines a credit loss as “all cash shortfalls”, which may imply that an entity should include all cash shortfalls in ECL measurement irrespective whether they are due to credit-related reasons. On the other hand, the objective and underlying concept of the ECL model (e.g. significant increase in credit risk, risk of default and credit impaired) seem to imply that the measurement of ECL should only be driven by credit-related factors.

Some respondents considered that the IFRS Interpretations Committee may have clarified this issue in its Agenda Decision Lessor Forgiveness of Lease Payments (IFRS 9 and IFRS 16) by concluding that the lessor, who voluntarily forgives certain lease payments due by the lessee, should include the anticipation of forgiving lease payments due into the measurement of ECL of the operating lease receivable to reflect “all cash shortfalls”. However, other respondents considered that the Agenda Decision has created further uncertainty about the boundaries of credit risk.

We considered that the meaning of “credit loss” is not only fundamental to the ECL assessment but is also closely related to the issue of the boundaries between the requirements on modification of financial assets and ECL (see below). In light of the ongoing concern in the market, we recommend that the IASB undertake proper standard-setting activities to clarify the meaning of “credit loss” in IFRS 9, i.e. whether it is based on an assessment of “all cash shortfalls” or “shortfalls as a result of an inability to pay”. We also recommend the IASB conduct a thorough review of IFRS 9 to ensure that the related concepts and terminologies applied in the ECL measurement align with the clarified meaning of “credit loss” within the context of IFRS 9.

Interaction of the ECL requirements with the requirements on modification and derecognition in IFRS 9

IFRS 9 does not contain clear guidance on how the requirements for modification and ECL interact with each other. Specifically, following a modification that does not result in derecognition, it is unclear how an entity should account for the ECL and the effect of the modification. Questions arise as to whether certain losses should be treated as impairment losses, write-offs, or modification losses. The uncertainty about the boundaries between the requirements for modification and ECL is further exacerbated by the unclear meaning of “credit loss” as mentioned earlier (“all cash shortfalls” or “shortfalls as a result of an inability to pay”).

In our submission to the IASB on PIR of IFRS 9 – Classification and Measurement, we expressed significant concerns regarding the modification requirements. Due to insufficient guidance in IFRS 9, different entities have developed varying accounting policies to assess whether a modification results in derecognition. The lack of clarity affects whether a modification would lead to derecognition of the original financial asset and recognition of a new one, resulting in a reset of initial credit risk and hence stage classification for ECL measurement. This is in contrast to cases where the modification does not result in derecognition, and the modified financial assets would be classified as stage 2 if the credit risk has increased significantly.

We note that the IASB has added a standard-setting project to its research pipeline on Amortized Cost Measurement, which will consider the modification of financial instruments. In this regard, we strongly recommend the IASB include the interaction of the modification and ECL requirements within the scope of that project and commence the project as soon as practicable.

Accounting for financial guarantee contracts

Financial guarantee contracts (FGCs) are widely used financial instruments in Mainland China and Hong Kong. However, we noted several application issues relating to the accounting for FGCs and recommend that the IASB provide guidance or clarification on how the relevant requirements in IFRS 9 should be applied. These issues include:

- From the holder’s perspective: There is a potential inconsistency between IFRS 9: B5.5.55 and the discussions by the IFRS Transition Resource Group for Impairment of Financial Instruments in terms of what “integral” means when assessing whether cash flows from FGCs are integral to the contractual terms for ECL measurement. This raises concerns on how to appropriately perform the integral assessment, particularly when the FGC is not mentioned in the contractual terms or the FGC is obtained for a revolving pool of receivables.

- From the issuer’s perspective: IFRS 9 does not provide application guidance on how the extant requirements for subsequent measurement in IFRS 9:4.2.1(c) are applied to FGCs with premiums received over time, leading to diversity in practice. In addition, questions have also been raised as to how the two amounts recognized under IFRS 9:4.2.1(c), namely the amortization amount determined based on IFRS 15 and the ECL allowance, interact with each other and hence how they should be presented in the statement of profit or loss.

This article was contributed by Carrie Lau and Kennis Lee, Associate Directors of the Institute’s Standard Setting Department. Visit our “What’s new” webpage for our latest publications, and follow us on LinkedIn for upcoming activities.