In July 2021, the International Auditing and Assurance Standards Board (IAASB) issued an exposure draft for a “simplified” auditing standard, the Proposed International Standard on Auditing for Audits of Financial Statements of Less Complex Entities (ISA for LCE). The IAASB's proposal and the Institute’s responses were discussed in previous A Plus articles from 2021 and 2022.

In December 2023, the IAASB released the final ISA for LCE, which is a new stand-alone auditing standard for auditors of less complex entities (LCEs). The ISA for LCE contains all requirements necessary to obtain reasonable assurance about whether the financial statements of an LCE, as a whole, are free from material misstatements, whether due to fraud or error.

In April 2025, the Hong Kong Institute of CPAs’ Auditing and Assurance Standards Committee (AASC) adopted the ISA for LCE as the Hong Kong Standard on Auditing for Audits of Financial Statements of Less Complex Entities (HKSA for LCE or the “standard”). To apply the HKSA for LCE in an audit engagement, the auditor must assess whether the entity meets the eligibility criteria outlined in the Authority in Part A of the standard.

Authority for using the standard

The Authority that governs the use of the HKSA for LCE is structured into three key categories, each of which must be met for the standard to be applied. To ensure the standard is appropriately applied in Hong Kong context, the AASC has introduced local refinements to these categories. Each category and their local refinements are described below.

Specific prohibitions

This category sets out classes of entities that are prohibited from using the standard in their audit engagements. They are:

- Law or regulation that prohibits the use of the HKSA for LCE or specifies the use of auditing standards other than the HKSA for LCE for the audit of the financial statements in that jurisdiction.

- The entity is a listed entity.

- The entity carries on any banking business and is an authorized institution as defined under the Banking Ordinance.

- The entity carries on any insurance business and is an authorized insurer as defined under the Insurance Ordinance.

- The entity is a licensed corporation under Part V of the Securities and Futures Ordinance to carry on a business in any regulated activity within the meaning of that Ordinance.

- The entity is granted an insurance broker company licence under Section 64ZA of the Insurance Ordinance to carry on regulated activities in one or more lines of business, and to perform the act of negotiating or arranging an insurance contract as an agent of any policy holder or potential policy holder.

- The entity is a public interest entity defined in Part 4A, Chapter A of the HKICPA Code of Ethics for Professional Accountants.

- The audit is an audit of group financial statements and (i) any of the individual entities or business units in the group do not qualify for using the HKSA for LCE as described above, or (ii) component auditors are involved, except when their involvement is limited to circumstances regarding a physical presence for a specific audit procedure for the group audit.

Qualitative characteristics

Qualitative characteristics describe the typical nature and circumstances of an audit of an LCE for which the standard includes all necessary requirements. If an entity does not exhibit these characteristics, it would ordinarily be precluded from using the HKSA for LCE for its financial statements audit.

Quantitative thresholds

These thresholds are established by relevant local bodies with standard-setting authority to determine eligibility for using the standard in each jurisdiction. In Hong Kong context, an entity or group must not exceed any two of the following limits to qualify for applying the HKSA for LCE in the relevant audit engagement:

- Total revenue of HK$200 million.

- Total assets of HK$200 million at the end of the reporting period.

- 100 employees.

The standard also sets out principles for assessing whether these quantitative thresholds are met, ensuring consistent and appropriate application in practice.

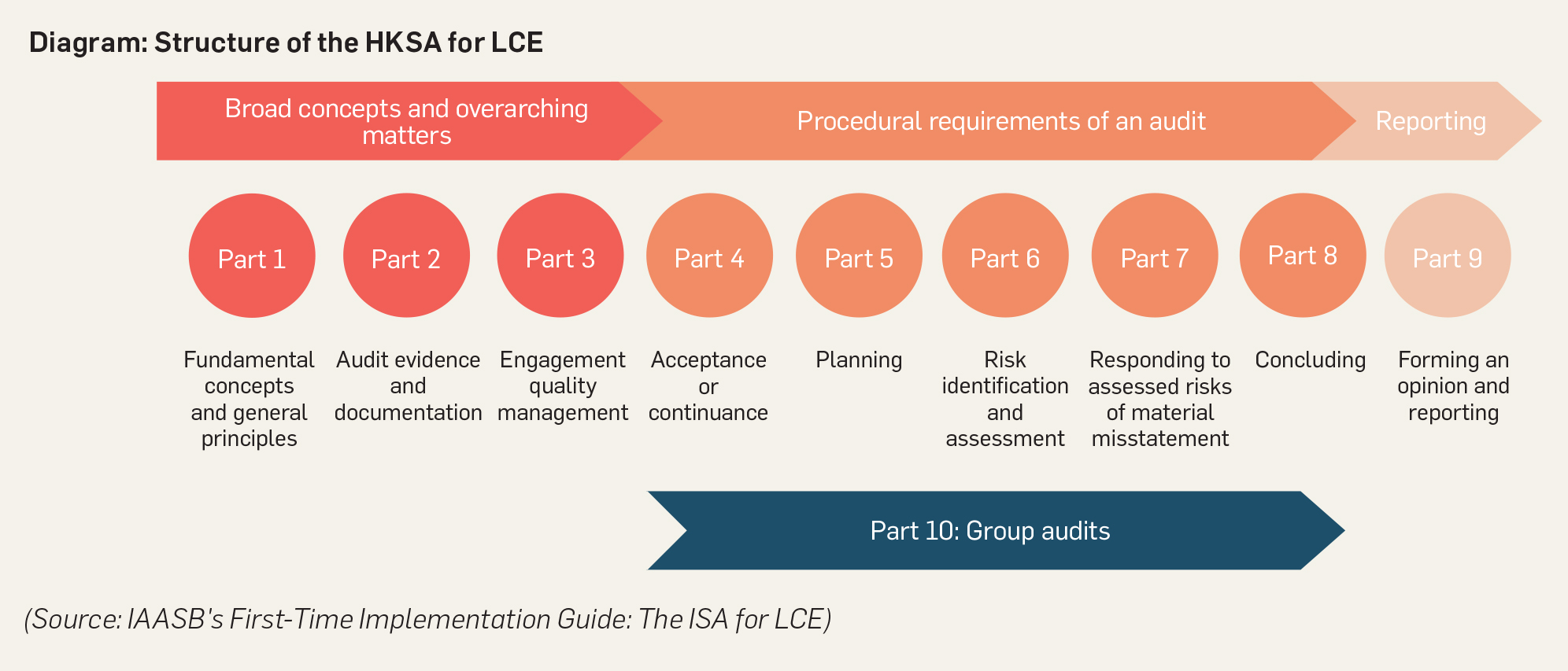

Overall design of the HKSA for LCE

The HKSA for LCE utilizes a risk-based approach to an audit, with requirements that are principles-based. The standard has been grouped into 10 parts that follow the flow of an audit. The parts are preceded by a Preface to the standard and its Authority (see the diagram below).

The requirements and Essential Explanatory Material (EEM) in the HKSA for LCE are designed to be proportionate to an audit of an LCE. Requirements and EEM in the standard do not address complex matters or circumstances. If the HKSA for LCE is used for an audit outside the intended scope of this standard, compliance with the requirements of the HKSA for LCE will not be sufficient for the auditor to obtain sufficient appropriate audit evidence to support a reasonable assurance opinion.

If an objective in a part of the standard cannot be achieved, the auditor shall evaluate whether this prevents the auditor from achieving the overall objectives of the auditor and thereby requires the auditor to: (a) modify the terms of engagement and perform the audit and report in accordance with the Hong Kong Standards on Auditing (HKSA); or (b) modify the auditor’s opinion or withdraw from the engagement (where withdrawal is possible under applicable law or regulation). Failure to achieve an objective represents a significant matter requiring documentation.

The EEM serves a similar purpose to application and other explanatory material in the HKSA but is targeted at a higher, conceptual and contextual level, taking into account the typical nature and circumstances of audits for which the standard has been designed. The EEM has been presented in italics and is highlighted in light blue. The EEM does not impose or expand requirements; rather, it provides explanation or guidance that is integral to understanding the relevant requirements.

Tailoring auditor’s reports under the HKSA for LCE

Auditors applying the HKSA for LCE in audit engagements should ensure that auditor’s reports are appropriately tailored to the specific reporting framework.

- For financial statements prepared under a fair presentation framework (e.g. HKFRS Accounting Standards; HKFRS for Private Entities Accounting Standard), refer to the illustration in paragraph 9.4 of the standard.

- For financial statements prepared under a compliance framework (e.g. HKICPA Small and Medium-sized Entity Financial Reporting Framework and Financial Reporting Standard (SME-FRF & FRS)), tailor the auditor’s report in accordance with paragraph 9.3.1 and footnote 39 of the standard. The Institute is currently developing an illustrative auditor’s report under the HKSA for LCE for audits of financial statements under the SME-FRF & FRS.

- For other scenarios, refer to the IAASB ISA for LCE Auditor Reporting Supplemental Guidance for guidance.

Implementation support

The HKSA for LCE will be effective for audits of financial statements of LCEs for periods beginning on or after 15 December 2025.

The Institute’s Basis for Conclusions summarizes the considerations of the AASC in making the local refinements to the Authority of the standard, along with an impact analysis of key areas that auditors should be aware of when applying the HKSA for LCE in audit engagements.

Additionally, the AASC has developed a Frequently Asked Questions document that addresses various scenarios related to the assessment of quantitative thresholds and provides local application guidance. Other relevant guides and materials are available at the Institute’s dedicated resource centre.

This article was contributed by the Institute’s Standard Setting Department.