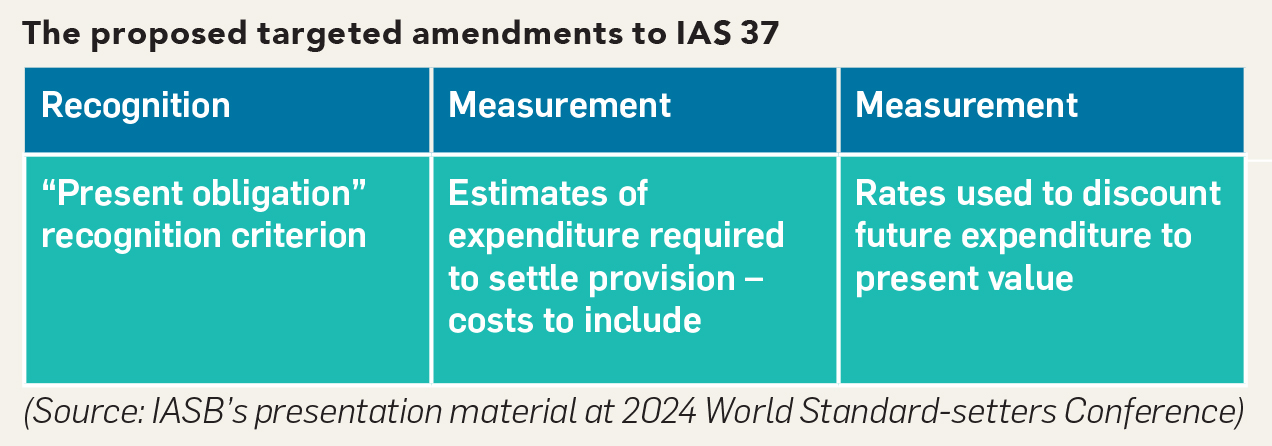

In November 2024, the International Accounting Standards Board (IASB) published an Exposure Draft (ED) proposing targeted amendments to International Accounting Standard (IAS) 37 Provisions, Contingent Liabilities and Contingent Assets. The proposed targeted amendments, which cover the three aspects of IAS 37 outlined in the diagram below, aim to clarify whether provisions need to be recognized, and if so, when to recognize them, as well as how to measure them.

The Institute responded to the ED in March this year. This article highlights our major comments on the ED. The full response is available on our website.

We appreciate the IASB’s endeavours in formulating proposals that aim at improving the requirements in IAS 37 for recognizing and measuring provisions. However, we have concerns in the following areas.

Transfer condition

We are concerned that paragraph 14L of the ED introduces new concepts of “transfer” and “exchange” of economic resources into IAS 37, which are neither defined in the Glossary nor elaborated upon further in IAS 37. Some respondents questioned whether typical payments, such as levies, are considered as “transfer” or “exchange” of economic resources under the ED. Others expressed concerns that in situations where the nature of the transaction is unclear, the ambiguity surrounding the definitions of “transfer” and “exchange” could create challenges in determining whether the transfer condition is met, and thus whether a present obligation exists.

To enhance clarity and support consistent application, we strongly recommend that the IASB clarify these concepts in IAS 37. This could be achieved by incorporating the principle of considering any future economic benefits of the asset or service received as a result of payment, as illustrated in Examples 3, 7 and 11B in the Guidance on implementing IAS 37 (Guidance), into the body of IAS 37.

Past-event condition

We have significant concerns regarding the proposed requirements for the past-event condition in paragraphs 14O to 14Q of the ED. The ED lacks clarity on how these paragraphs interact and how they apply to scenarios involving multiple conditions. Additionally, the application of the concepts introduced in these paragraphs to certain illustrative examples in the Guidance is confusing. For instance, it is unclear why the outcomes of Examples 13B and 13C are different (two separate actions versus one action) when they illustrate similar fact patterns.

Determining what constitutes an “action” under these paragraphs becomes particularly challenging in complex fact patterns involving multiple conditions in a contract or legislation. This complicates an entity’s assessment of whether the conditions represent one action, two (or more) separate actions, a continuation of an activity, or a measurement base for the provision. As a result, it is unclear whether paragraphs 14O, 14P or 14Q of the ED should be applied, which would affect the timing of recognizing the provision.

In light of the above, we strongly recommend that the IASB clearly illustrate the interaction between paragraphs 14O to 14Q in the final amendments, particularly whether, and if so, which requirement would take precedence if they are relevant to the same fact pattern. Furthermore, we recommend that the IASB enhance the relevant illustrative examples in the Guidance to ensure consistent application of the proposed requirements across different fact patterns. We also recommend that the IASB test these proposals further to understand their impact and assess whether the outcomes are appropriate.

Measurement – Future operating costs

The ED proposes deleting paragraph 18 of IAS 37, which specifies that no provision is recognized for costs that need to be incurred to operate in the future, without explanation in the Basis for Conclusions. This creates confusion regarding whether future operating costs should be included in measuring a provision under the proposed paragraph 40A of the ED when those costs are directly related to settling the obligations. We believe that the IASB does not intend to change this general measurement principle which is applicable for all types of provisions. Therefore, we strongly recommend that the IASB either reinstate this paragraph or clearly specify this principle in the “measurement” section of the final amendments.

Other recommendation

As noted above, although this ED is characterized by the IASB as targeted improvements or clarifications, it may have a broader impact on current accounting practices than initially anticipated. To ensure a comprehensive understanding of the potential effects of the ED, we recommend that the IASB conduct further outreach with stakeholders when developing the final amendments.

This article was contributed by George Au and Shiro Lam, Associate Directors of the Institute’s Standard Setting Department.