Background

Hong Kong Accounting Standard (HKAS)/ International Accounting Standard (IAS) 1 Presentation of Financial Statements specifies the requirements of how entities classify liabilities as current or non-current.

In 2020, the International Accounting Standards Board (IASB) issued amendments to IAS 1 Classification of Liabilities as Current or Non-current (2020 Amendments) which clarified certain aspects of how entities classify liabilities as current or non-current. One of the key amendments relates to the classification of liabilities subject to covenants. In particular, the amendment specified that if an entity’s right to defer settlement of a liability is subject to compliance with specified conditions, the right exists at the end of the reporting period only if the entity complies with those conditions at the end of the reporting period.

Stakeholders were concerned about the impact of this amendment and as a result, the IFRS Interpretations Committee (IC) published a tentative agenda decision explaining how to apply the amendment to particular fact patterns. Respondents to the tentative agenda decision raised concerns about the outcomes and potential consequences of the amendment in some situations. The IC reported this feedback to the IASB, highlighting new information that the IASB had not considered when developing the amendment. Having considered the new information, the IASB issued further amendments to IAS 1 Non-current Liabilities with Covenants (2022 Amendments) in 2022.

The Institute issued the equivalent 2020 and 2022 Amendments in August 2020 and December 2022, respectively. At the same time, the Institute also updated Hong Kong Interpretation 5 (Revised) Presentation of Financial Statements – Classification by the Borrower of a Term Loan that Contains a Repayment on Demand Clause (HK Int 5) to incorporate the references to the 2020 and 2022 Amendments. The conclusions in HK Int 5 are not impacted by these amendments.

What’s new compared to the existing requirements in HKAS 1?

The key changes from the current HKAS 1 due to the 2020 and 2022 Amendments are summarized as follows:

Right to defer settlement for at least 12 months

The word “unconditional” has been removed from paragraph 69 of HKAS 1 so that this paragraph no longer refers to an “unconditional” right to defer settlement. A new paragraph has been added which requires that an entity’s right to defer settlement for at least 12 months after the reporting period must have substance and exist at the end of the reporting period.

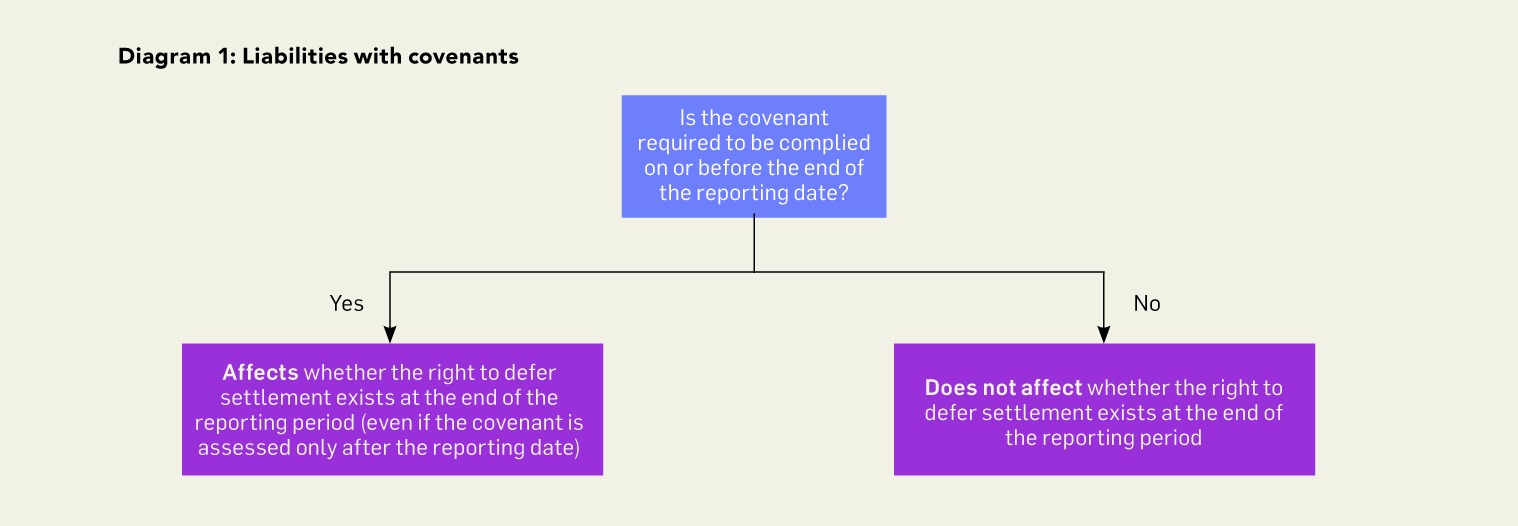

Liabilities with covenants

An entity’s right to defer settlement may be subject to its compliance with covenants specified in a loan arrangement. The 2022 Amendments clarify that covenants with which an entity must comply after the reporting date do not affect the classification of a liability as current or non-current at the reporting date. However, covenants with which an entity is required to comply on or before the reporting date affect the classification, even if the covenant is assessed only after the entity’s reporting date. See Diagram 1 below.

Management’s expectations

The 2020 Amendments explicitly clarify that a liability’s classification as current or non-current is unaffected by management’s intentions or expectations about whether an entity will exercise its right to defer settlement of the liability for at least 12 months after the reporting period.

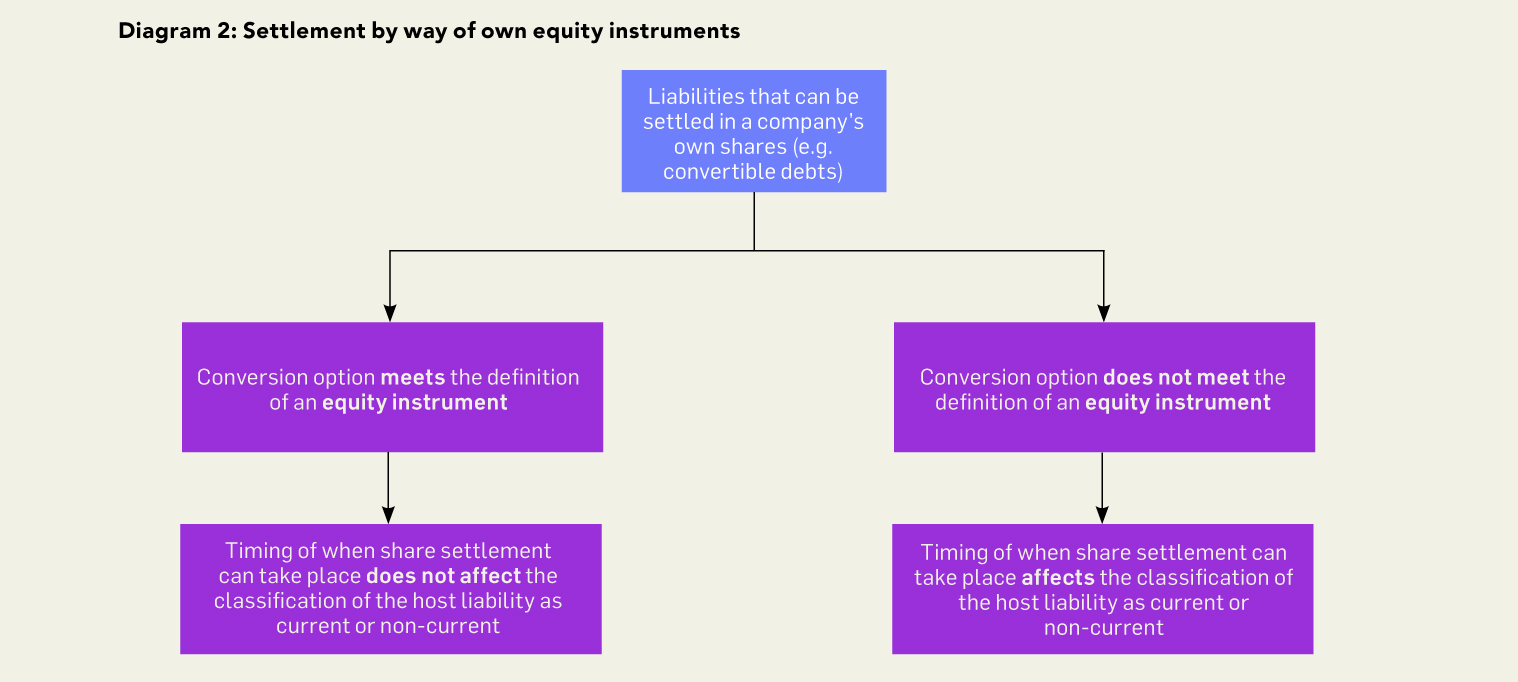

Settlement by way of own equity instruments

The 2020 Amendments clarify the meaning of “settlement” for the purpose of classifying a liability as current or non-current. Settlement refers to a transfer to the counterparty that results in the extinguishment of the liability. The transfer could be of cash, goods or services, or the entity’s own equity instruments.

In addition, the amendments clarify how an entity classifies a liability that can be settled in its own equity instruments, e.g. convertible debt. If a liability has terms that could, at the option of the counterparty, result in its settlement by the transfer of the entity’s own equity instruments, these terms do not affect its classification as current or non-current if the conversion option is accounted for as equity under HKAS 32 Financial Instruments: Presentation. In other cases, the transfer of equity instruments would constitute settlement of the liability for the purpose of classifying it as current or non-current (e.g. if an obligation to transfer equity instruments is accounted for as a derivative). See Diagram 2 below and refer to section 10 of the Institute’s Financial Reporting, Auditing and Ethics Alert 37 Financial Reporting Considerations to Close Out 2020 for examples.

Disclosure requirements

The 2022 Amendments introduced additional disclosure requirements for non-current liabilities that are subject to future covenants. The disclosures aim to enable investors to assess the risk that the liabilities could become repayable within 12 months. These disclosures include i) information about the covenants with which the entity is required to comply; and ii) facts and circumstances, if any, that indicate the entity may have difficulty complying with the covenants.

Transition and effective date

Both the 2020 and 2022 Amendments are to be applied as a package and are effective for annual reporting periods beginning on or after 1 January 2024, with early adoption permitted. Entities will need to apply these amendments retrospectively in accordance with HKAS 8 Accounting Policies, Changes in Accounting Estimates and Errors.

Act now to assess the impact

Both the 2020 and 2022 Amendments affect only the presentation of liabilities as current or non-current in the statement of financial position and disclosure of liabilities in the notes to the financial statements, and not the recognition or measurement of these liabilities. However, the amendments could result in entities reclassifying some liabilities from current to non-current, and vice versa, potentially affecting those entities’ compliance with loan covenants. Consequently, entities are recommended to assess the potential impact of the amendments early, and if the amendments could result in the reclassification of certain liabilities from non-current to current, entities may want to consider renegotiating covenants or agreements with the banks or other financial institutions.

This article was contributed by Katherine Leung, Associate Director of the Institute’s Standard Setting Department. Visit our “What’s new” webpage for our latest publications, and follow us on LinkedIn for upcoming activities.