The International Accounting Standards Board (IASB) initiated the Primary Financial Statements (PFS) project in response to investors' concerns about the comparability and transparency of companies’ performance reporting. The IASB has recently completed its technical work on the PFS project and expects to publish a new International Financial Reporting Standard (IFRS) Accounting Standard, IFRS 18 Presentation and Disclosure in Financial Statements, in Q2 2024. IFRS 18 will set out the requirements for the presentation and disclosure of information in financial statements and will replace International Accounting Standard (IAS) 1 Presentation of Financial Statements. IFRS 18 will be effective for annual reporting periods beginning on or after 1 January 2027, with restatement of the comparative period being required.

Who will be impacted by the new standard?

All stakeholders in all industries that apply IFRS Accounting Standards will be impacted. The changes introduced by IFRS 18 will affect how entities present and disclose information in the financial statements, the information available to investors, and the extent of information subject to assurance by auditors.

What will be changed?

IFRS 18 introduces significant changes to the presentation of financial statements, with a focus on the statement of profit or loss. Nonetheless, certain requirements of IAS 1 will be included in IFRS 18 with minimal changes. As the final version of IFRS 18 has not yet been released, the following overview of key changes from IAS 1 to IFRS 18 is based on the IASB’s tentative decisions and may differ from the final requirements of IFRS 18.

Categories and subtotals

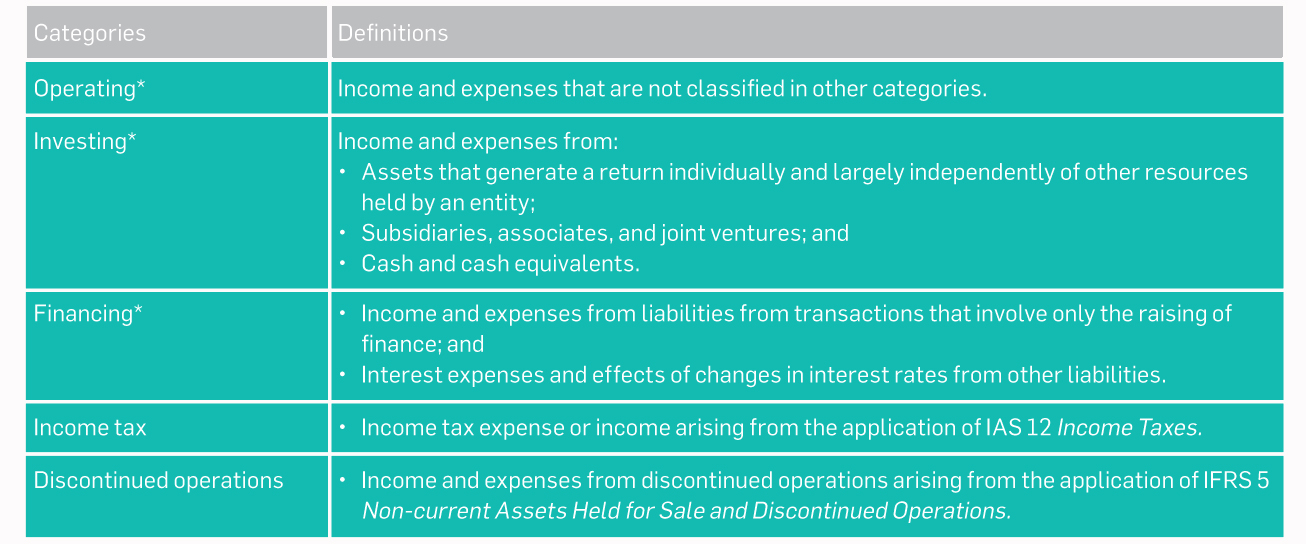

IAS 1 does not require income and expenses to be classified into particular “classes” or “categories” nor does it mandate the presentation of any subtotals between “revenue” and “profit or loss” in the statements of profit or loss. To enhance consistency and comparability of companies’ financial performance, IFRS 18 will require income and expenses to be classified into five categories in the statement of profit or loss. See table 1.

Table 1: Income and expenses that is required to be classified into five categories in the statement of profit or loss

* The classification of income and expenses may differ in some cases for entities with specified main business activities, i.e. entities that provide financing to customers (e.g. banks) or invest in assets as their main business activities (e.g. insurance and investment entities).

Furthermore, all entities will be required to present two new subtotals:

- Operating profit or loss, which comprises all income and expenses classified in the operating category; and

- Profit or loss before financing and income tax, which comprises all income and expenses classified in the operating and investing categories.

Management-defined performance measures (MPM)

IFRS 18 will include specific disclosure requirements for MPM to improve the transparency of measures entities provide and the discipline with which they are prepared. MPM are subtotals of income and expenses, other than subtotals specified by IFRS Accounting Standards, that an entity (a) uses in public communications outside financial statements; and (b) uses to communicate to users of financial statements management’s view of an aspect of the entity’s financial performance. Examples of MPM include adjusted profit and adjusted earnings before interest, taxes, depreciation, and amortization.

IFRS 18 will require entities to disclose the following information about their MPM in a single note:

- A statement that the MPM provides management’s view;

- An explanation of the MPM calculation and why it provides useful information;

- A reconciliation to the most directly comparable specified subtotal or total; and

- An explanation of any changes to the MPM.

Labelling, aggregation and disaggregation

IFRS 18 will enhance the requirements for labelling, aggregation and disaggregation with the following key changes:

- Items must be disaggregated if the resulting disaggregated information is material;

- Use the label “other” only if an entity is unable to find a more informative label; and

- Entities that classify expenses by function will be required to disclose the amounts included in each line item for depreciation, amortization, employee benefits, impairment losses and write-down of inventories.

Statement of cash flows

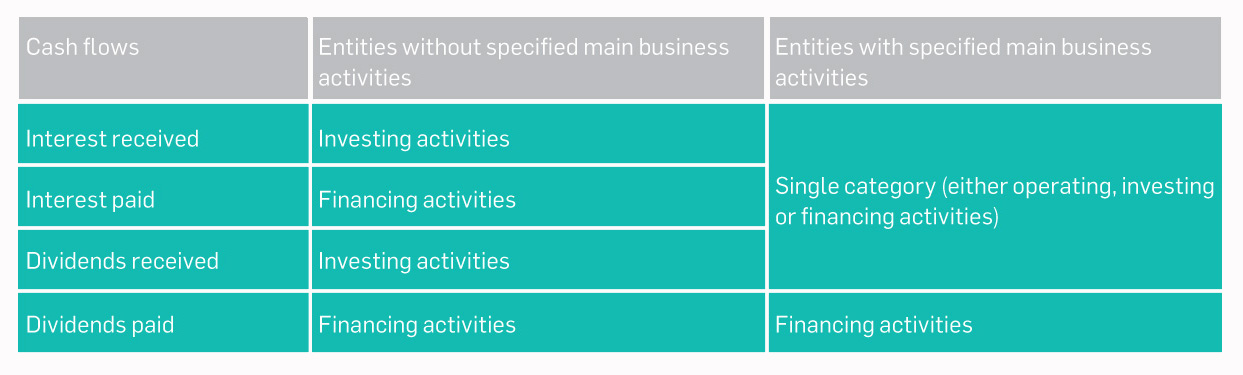

There will be consequential amendments to IAS 7 Statement of Cash Flows to improve comparability. The amendments will include:

- The newly introduced mandatory subtotal, operating profit or loss, will be the starting point for the indirect method of reporting cash flows from operating activities; and

- The elimination of accounting policy choice to classify interest and dividend cash flows. Entities will be required to classify their interest and dividend cash flows according to the new requirements. See table 2.

Table 2: Classification of interest and dividend cash flows according to the new requirements

What should entities do now?

Given the potential implications of the new standard, the following are some suggested steps that entities should take now.

- Understand what the forthcoming accounting requirements are. The IASB project webpage provides a preliminary overview of what the tentative standard will look like.

- Conduct an initial assessment of how the new requirements will impact your entity’s financial reporting systems, processes and controls.

- Review the policy to aggregate, disaggregate and label information based on the new requirements.

- Consider the potential impact of the new requirements about MPM on your entity’s external communication strategy.

- Stay tuned for the forthcoming publication of IFRS 18 and keep an eye on our Presentation and Disclosure in Financial Statements webpage, which will provide you with access to useful technical support and updates from both the IASB and the Institute.

This article was contributed by Katherine Leung, Associate Director and Sam Chan, Manager of the Institute’s Standard Setting Department.