In July, the Institute issued Hong Kong Financial Reporting Standard (HKFRS) 18 Presentation and Disclosure in Financial Statements, the equivalent of International Financial Reporting Standard (IFRS) 18 Presentation and Disclosure in Financial Statements issued by the International Accounting Standards Board (IASB). HKFRS 18 replaces Hong Kong Accounting Standard (HKAS) 1 Presentation of Financial Statements. It introduces new requirements that affect all entities in all industries as to how they present and disclose financial performance in financial statements. Requirements in HKAS 1 that are unchanged have been transferred to HKFRS 18 and other HKFRSs. HKFRS 18 is effective for annual periods beginning on or after 1 January 2027, but entities can apply it earlier. Entities are required to apply HKFRS 18 retrospectively.

Key new requirements in HKFRS 18

HKFRS 18 introduces three sets of new requirements to improve entities’ reporting of financial performance and give investors a better basis for analysing and comparing entities.

1. Statement of profit or loss

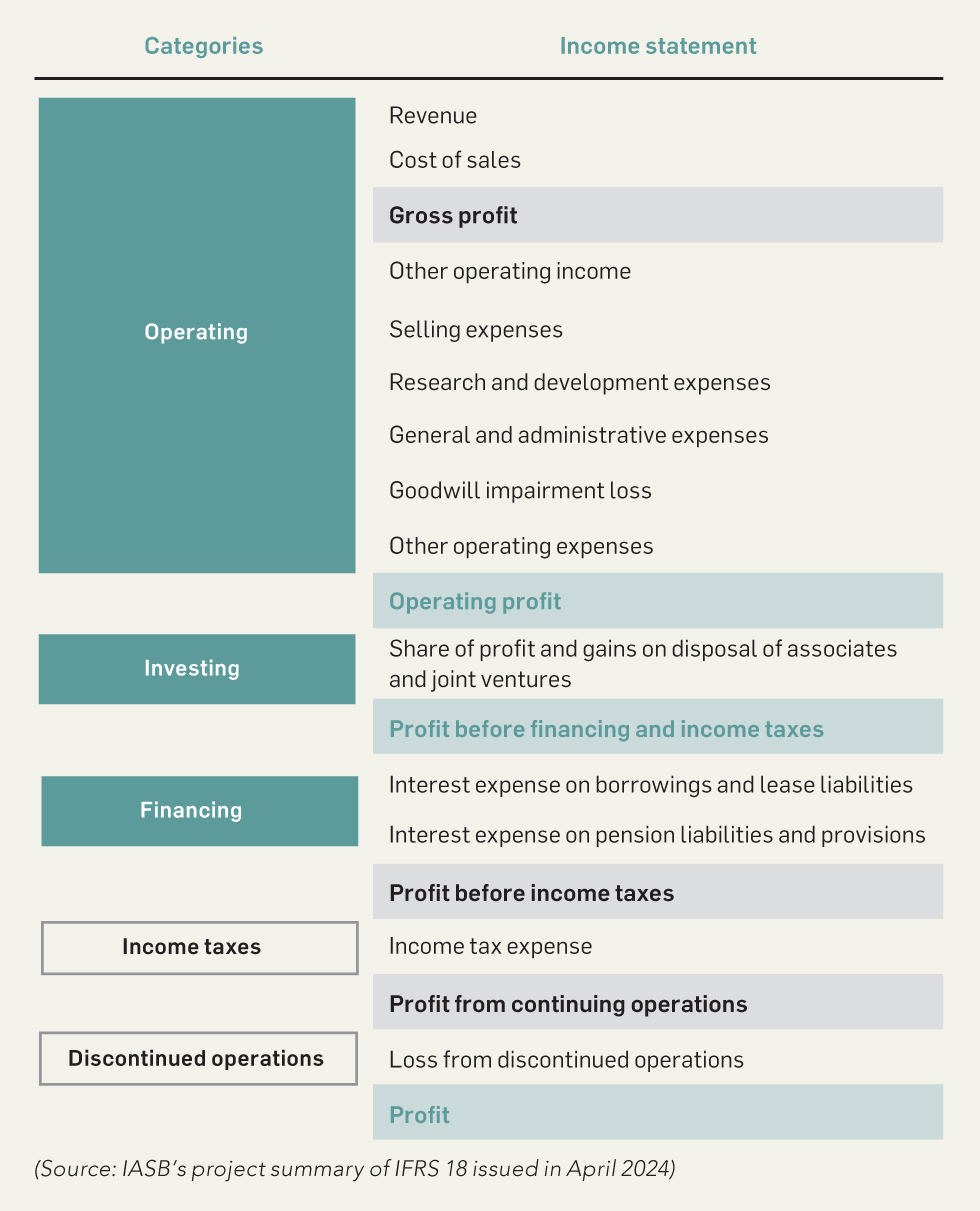

To improve the structure of the statement of profit or loss, HKFRS 18 introduces three new defined categories: operating, investing and financing (the categories in the statement of profit or loss have different meanings to those in the statement of cash flows) for classifying income and expenses, and requires entities to present two new defined subtotals (operating profit and profit before financing and income taxes).

The operating category is the default category and consists of all income and expenses that are not classified in any of the other categories. This means that the operating category includes, but is not limited to, income and expenses from an entity’s main business activities regardless of whether they are volatile or non-recurring.

The investing category includes income and expenses from assets that generate returns separately from an entity’s business activities, and from cash and cash equivalents as well as investments in associates, joint ventures and unconsolidated subsidiaries.

Examples of income and expenses that will be classified in the investing category are:

- Share of profit of associates and joint ventures accounted for using the equity method;

- Rental income and fair value gains or losses of investment properties;

- Interest income and fair value changes on debt securities; and

- Dividends and fair value changes on equity investments.

The financing category includes income and expenses on liabilities arising from transactions that involve only the raising of finance, such as bank loans and bonds, and interest expenses on any other liabilities, such as lease and pension liabilities.

The diagram below shows the structure of, and subtotals in, a statement of profit or loss for most entities that do not have a specified main business activity and present some operating expenses by function and some by nature.

Diagram: Statement of profit or loss for most entities

Entities with specified main business activities

HKFRS 18 includes additional classification requirements for entities with specified main business activities, i.e. entities that provide financing to customers (e.g. banks) or that invest in assets as a main business activity (e.g. insurers, real estate companies). Such entities would classify in the operating category the income and expenses that would otherwise be classified in the investing or financing categories by most entities. HKFRS 18 also includes accounting policy choices regarding the classification of certain income and expenses for entities with specified main business activities.

Classification of specific income and expenses

Foreign exchange differences

HKFRS 18 requires entities to classify foreign exchange differences in the same category of the statement of profit or loss as the income and expenses from the items that gave rise to the foreign exchange differences. For example, foreign exchange differences on bank loans are classified in the financing category. If classifying foreign exchange differences this way involves undue cost or effort, entities are permitted to classify foreign exchange differences in the operating category.

Other specific income and expenses

HKFRS 18 also includes specific requirements for classifying fair value gains and losses on derivatives, and income and expenses from hybrid contracts. The classification of fair value gains and losses on derivatives depends on whether the derivatives are used to manage exposure to identified risks and whether they are designated as hedging instruments. The classification of income and expenses from hybrid contracts comprising host liabilities and embedded derivatives depends on whether the embedded derivative is separated from the host liability and the nature of the hybrid contract.

Impact on entities

- The classification of income and expenses varies depending on an entity’s main business activities. Entities will need to carefully assess their main business activities and consider whether they are engaged in specified main business activities.

- Entities will then need to analyse the structure of their statement of profit or loss and assess how their current presentation may need to change.

- Entities with large volumes of derivatives and foreign currency-denominated items may incur additional costs and efforts to classify foreign exchange differences and derivatives in the relevant categories of the statement of profit or loss.

- Entities may need to make decisions on their accounting policies in some cases, e.g. the classification of certain income and expenses for entities with specified main business activities.

- The change of the structure of statement of profit or loss may impact entities’ current reporting practices, internal processes and accounting systems.

2. Management-defined performance measures (MPMs)

HKFRS 18 defines MPM as a subtotal of income and expenses other than those listed by HKFRS 18 or specifically required by HKFRSs, that an entity uses in public communications outside financial statements, and to communicate to investors management’s view of an aspect of the financial performance of the entity as a whole. Examples of MPM include adjusted profit, adjusted operating profit, adjusted earnings before interest, taxes, depreciation and amortization.

HKFRS 18 requires entities to disclose MPMs in a single note, including:

- A reconciliation between the measure and the most directly comparable subtotal listed in HKFRS 18 or total or subtotal specifically required by HKFRSs, including the income tax effect and the effect on non-controlling interests for each item disclosed in the reconciliation;

- A description of how the measure communicates management’s view and how the measure is calculated;

- An explanation of any changes in the entity’s MPMs or in how it calculates its MPMs; and

- A statement that the measure reflects management’s view of an aspect of financial performance of the entity as a whole and is not necessarily comparable to measures sharing similar labels or descriptions provided by other entities.

Impact on entities

- Entities that have been communicating with external users using “non-generally accepted accounting principles (GAAP)” measures will need to assess whether these non-GAAP measures meet the definition of MPMs, which will now be reported in the financial statements and subject to audit.

- Entities that already communicate using measures that are MPMs are likely to incur costs in providing the reconciliation and determining the income tax effect and the effect on non-controlling interest for each adjusting item. Entities may need to develop or revise the internal processes they use for preparing the reconciliation.

- As a result of the new disclosure requirements, entities may want to revisit their external communication strategies using MPMs.

3. Grouping of information

HKFRS 18 provides guidance for entities on grouping transactions and other events into the line items in the primary financial statements and information disclosed in the notes. Entities are required to:

- Aggregate items that have similar characteristics, and disaggregate items that have different characteristics;

- Group items in a way that does not obscure material information or reduce the understandability of the information presented;

- Use meaningful labels or descriptions for aggregated items, and use the label “other” only when entities are unable to find a more informative label; and

- Place items in the primary financial statements and the notes to fulfil their complementary roles.

HKFRS 18 requires an entity to present the operating category expenses based on their nature or their function. Entities that present expenses classified by function are required to disclose in the notes the amount of depreciation, amortization, employee benefits, impairment losses and write-downs of inventories included in each line item in the operating category of the statement of profit or loss.

Impact on entities

- Entities will need to revisit and adjust their internal reporting systems and processes to ensure compliance with the aggregation and disaggregation requirements, as well as to capture relevant information to satisfy the additional disclosures on the five specified operating expenses by nature.

- Entities will need to use a more informative label for items labelled as “other” in the financial statements, e.g. other expenses/income, other receivables/payables, or to disclose further information about these items.

Other changes introduced by HKFRS 18

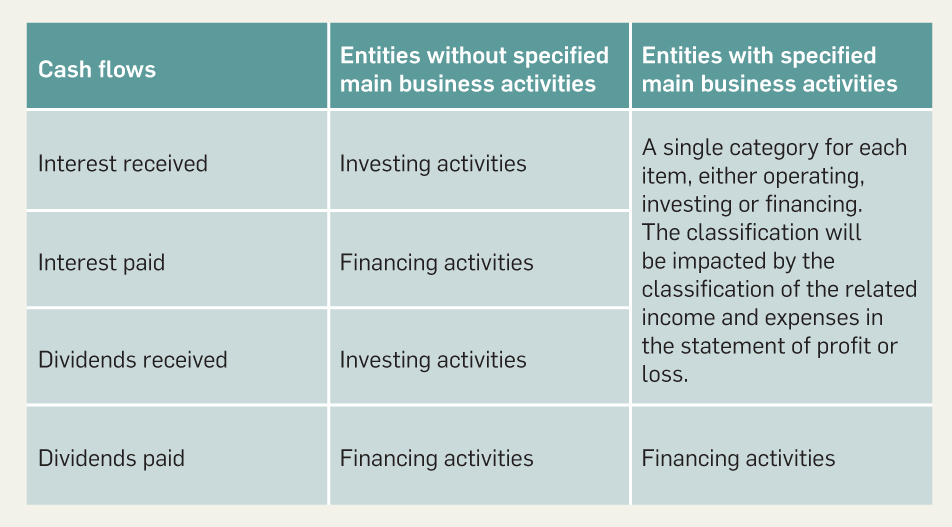

Certain narrow scope consequential amendments have been made to HKAS 7 Statement of Cash Flows to improve comparability. These amendments include:

- Requiring entities to use the operating profit subtotal as the starting point for reporting cash flows from operating activities using the indirect method; and

- Removing the accounting policy choices for classifying interest and dividend cash flows. Entities will classify their interest and dividend cash flows as shown in the table below.

Table: Classification of interest and dividend cash flows in the statement of cash flows

In addition, certain requirements from HKAS 1 have been moved to HKFRS 7 Financial Instruments: Disclosures and HKAS 8 Accounting Policies, Changes in Accounting Estimates and Errors. These requirements include:

- The disclosure requirements for puttable financial instruments classified as equity;

- The concepts of true and fair view and compliance with HKFRSs;

- Whether an entity is a going concern;

- The accrual basis of accounting; and

- Disclosure of an entity’s selection and application of accounting policies.

To better reflect the amended content of HKAS 8, the title of HKAS 8 will be changed to Basis of Preparation of Financial Statements.

Implementing HKFRS 18

The implementation of HKFRS 18 will have a broad impact across various entities and industries. To prepare for this change, entities are encouraged to start preparing for the implementation as soon as possible. Entities are advised to read the new standard thoroughly and assess its effect on their operations and reporting. The IASB has provided useful technical resources, such as illustrative examples, project summary and effects analysis, to support the implementation process. These materials, together with additional support from the Institute, are available on the Institute’s HKFRS 18 Presentation and Disclosure in Financial Statements webpage. Additionally, the Institute plans to offer educational sessions to help entities navigate the key aspects of the new requirements and the considerations for Hong Kong entities in general as well as for specific industries. Entities should stay tuned for these upcoming educational sessions and get in touch with the Institute’s Standard Setting Department through the Technical Enquiry system if they have any questions with implementing HKFRS 18.

This article was contributed by Katherine Leung, Associate Director of the Institute’s Standard Setting Department. Visit our “What’s new” webpage for our latest publications, and follow us on LinkedIn for upcoming activities.