The Greater Bay Area (GBA) initiative in China is one of the most important economic development plans in recent years to connect the 9+2 GBA cities in Southern China and the two special administrative regions to form an integrated economic and business zone. The central government realized that having the right talent to help develop the GBA economy is important, and proceeded to introduce tax incentives to attract high-calibre talent from overseas to work in the Mainland GBA cities. In March, the Ministry of Finance (MoF) and the State Taxation Administration (STA) issued Caishui [2019] No. 31 outlining the framework for Individual Income Tax (IIT) rebate for eligible overseas talent. In June, Yue Cai Shui [2019] No. 2 was issued to clarify details of the IIT rebates.

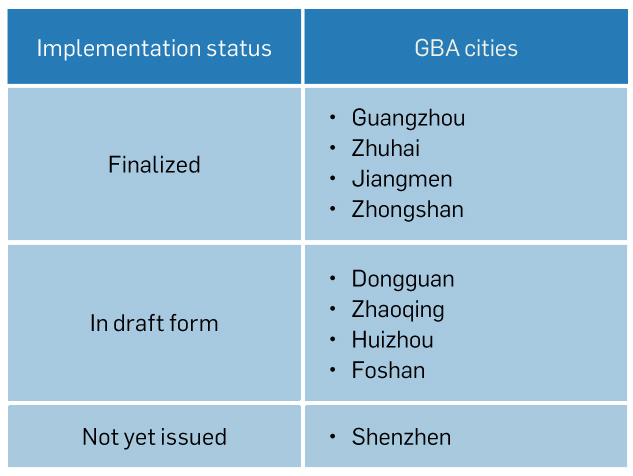

Since the core competencies and economic development focus of the nine Mainland GBA cities vary, these Mainland GBA cities have the autonomy to define the categories of “high-end talent” and “talent in short supply” with special skills to qualify for the IIT rebates. The status of the local implementation rules as of 17 September are summarized in Table 1.

Table 1: Local implementation rules as of 17 September 2019

IIT rebate calculation method and illustration

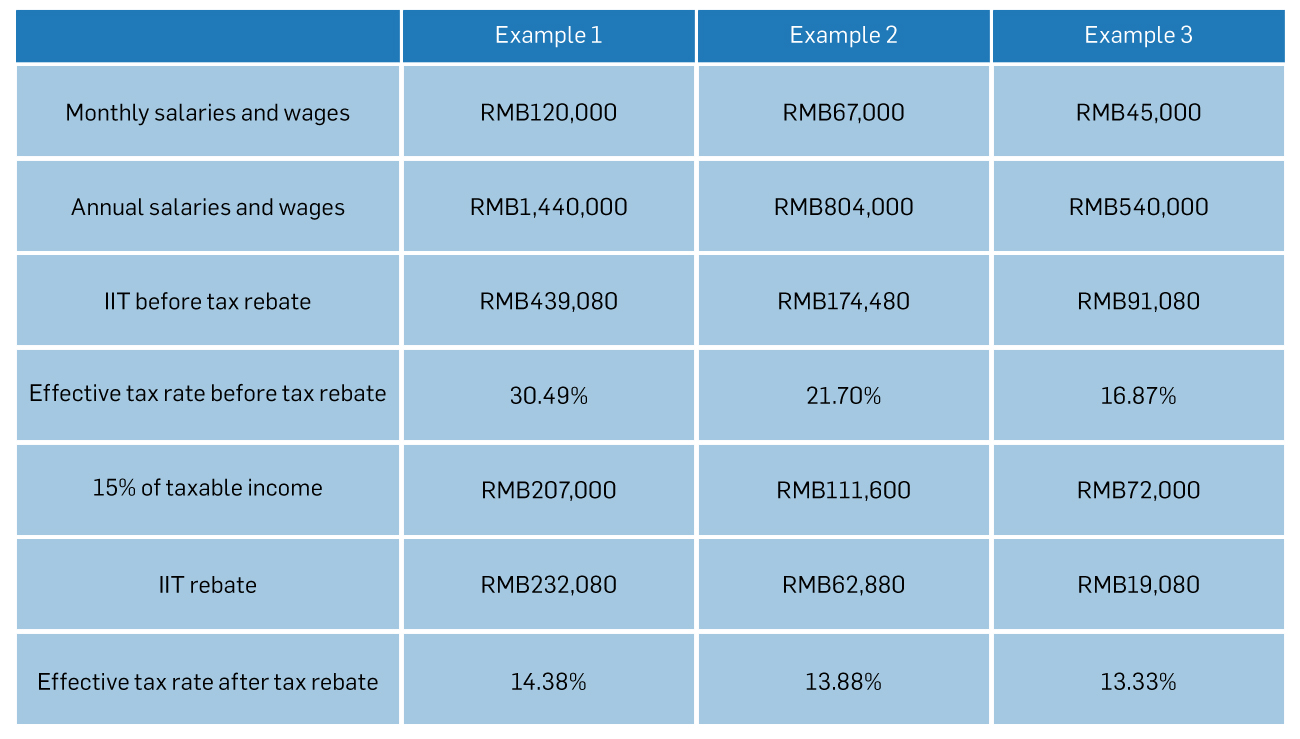

The IIT rebate applies to income from 1) salaries and wages; 2) remuneration of independent services; 3) author’s remuneration; 4) royalty income; 5) income from business operations; and 6) subsidies income obtained from selected talent projects or programmes. The rebate is calculated as the difference between the actual IIT paid by an individual and 15 percent of taxable income. Furthermore, the rebate will not be treated as taxable income in the hands of the taxpayers for IIT purposes. Table 2 considers the effect of the rebate on a range of salary income levels for an employee paying his own IIT, assuming the taxpayer is only entitled to the standard deduction of RMB60,000, no other deductions, and no other comprehensive income.

As illustrated in Table 2, the taxpayer would be subject to effective tax rates broadly on par with that in Hong Kong after receiving the tax rebates.

Table 2: Effective tax rates

Before implementation of the tax rebate policy in the Mainland GBA cities, individuals who are subject to IIT on a day apportionment basis would try to spend less time in China in order to reduce their IIT burden. Now with the IIT rebate, individuals who qualify can travel more freely between Hong Kong and the nine Mainland GBA cities from the total personal income tax burden point of view.

Some employers too will benefit. If employers offer their employees tax equalization benefits, the IIT rebate will mean a reduction of employment cost, as the equalization amount will be lower.

Despite the above, individuals should be aware that if they become tax residents for IIT purposes, they will be subject to IIT on their worldwide income. Foreign individuals who do not wish to become tax residents for IIT purposes can take a tax break by staying away from the Mainland China for more than 30 consecutive days in a tax year within six consecutive tax years. By virtue of the relevant provisions of Public Notice [2019] No. 34 jointly issued by the MoF and STA, they will not be subject to IIT on their worldwide income.

IIT rebate application criteria

The applicant must meet the following basic and additional conditions:

Basic conditions – All three must be met:

- Hong Kong or Macau permanent residents, Hong Kong residents under the Hong Kong immigration Admission Schemes for Talent, Professionals and Entrepreneurs, Taiwan residents, foreigners, or Chinese students or overseas Chinese who obtained long-term residency abroad.

- Work in one of the nine Mainland GBA cities and pay taxes according to the IIT law. According to the finalized local implementation rules, some GBA Mainland cities impose further qualifying conditions on this point. For instance, to qualify for IIT rebates in Guangzhou, Zhuhai and Jiangmen, the applicants must stay in the cities at least 90 days in a tax year. Moreover, it is provided specifically in the rules of Guangzhou and Jiangmen that overseas employees on secondment can also apply for the IIT rebate.

- Compliance with laws and regulations, ethics and integrity relating to scientific research.

Additional conditions – One must be met:

- Qualify as “high-end talent” or

- Qualify as “talent in short supply”

As the definitions of these categories vary among the nine Mainland GBA cities, an individual who qualifies as either in one Mainland GBA city does not necessarily mean that he meets the requirements for the other cities.

Will your employees benefit from the IIT rebate policy?

Mobility of talent in the GBA could be truly stirred up if the IIT rebate can benefit some of the employees where their physical work locations are a secondary consideration. To date, among the four sets of finalized local implementation rules, the Guangzhou rules provide a detailed list of both “high-end talent” and “talent in short supply.” The “talent in short supply” spans 16 industries with a wide spectrum of work types and seniority. However, the annual taxable income subject to IIT of the applicants in Guangzhou must be more than RMB300,000. The following is a selection of professions or positions included in the list:

- Chartered financial analyst

- Certified public accountant

- Private banker

- Insurance actuarial talents

- Risk management talents

- Fund manager

- Senior management (e.g. chairman, vice chairman, general manager, deputy general manager, director, chief economist, chief accountant, etc.)

- Software engineer

- Construction (including planner, designer, engineer, etc.)

- Professional service (including person with legal professional qualifications, registered surveyors, tax agents, translators, etc.)

- Product manager or project manager in new generation information technology industry

- New energy/new material engineer

- Electrician

- Logistics manager in modern e-commerce

- Performing artist

- Specialist doctor (e.g. pediatrician, obstetrician)

Can Chinese nationals benefit from the policy?

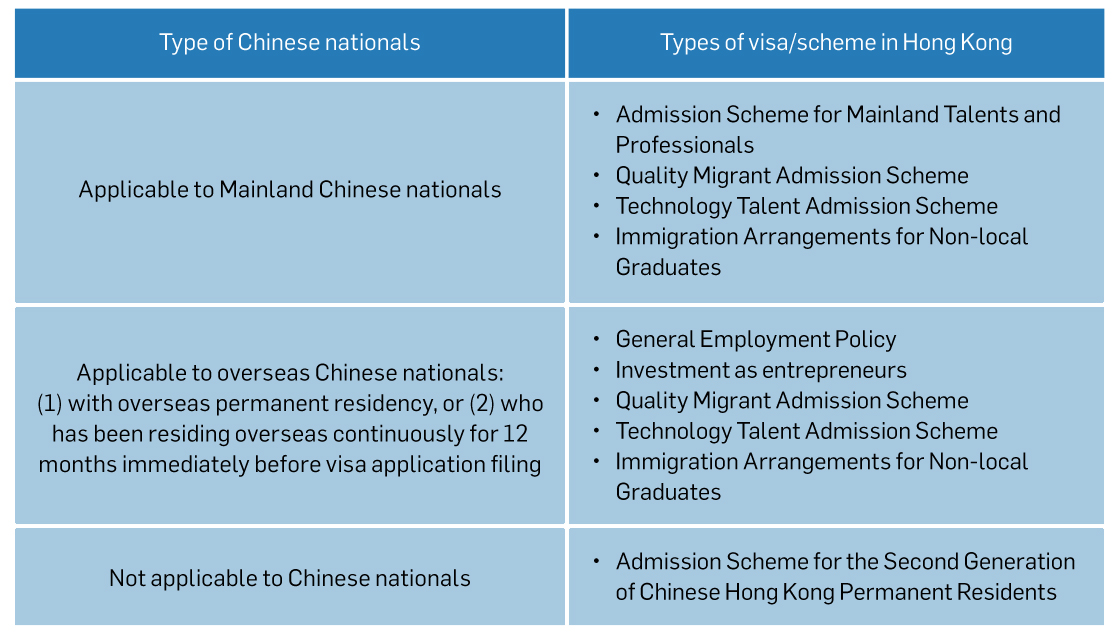

Chinese students or overseas Chinese who obtained long-term residency abroad are covered by the IIT rebate policy. In addition, as detailed in Table 3, Hong Kong residents under Hong Kong’s Admission Schemes for Talent, Professionals and Entrepreneurs which offers different types of visas, some of which are applicable to Chinese nationals. These individuals may qualify for the IIT rebates.

Table 3: Visa schemes for overseas Chinese nationals in Hong Kong

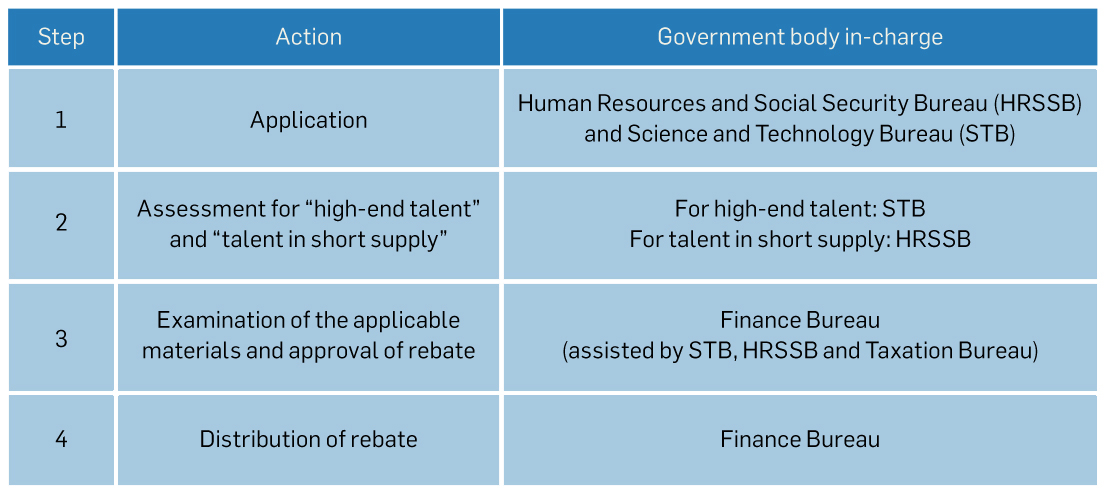

Indicative application procedures for the rebate

If the individual’s IIT is withheld by a withholding agent, the application for IIT rebate should preferably be submitted by the withholding agent on the individual’s behalf. In the absence of withholding agent, the applicant shall submit their application in person.

Table 4 illustrates the general application procedures and the government body in-charge for each step. Note that the process can vary among the nine Mainland GBA cities. For example, in Zhongshan, the assessment of “high-end talent” and “talent in short supply” is required before application for IIT rebate.

Table 4: General application procedures for IIT rebate

The rebate is calculated and distributed once a year. For those who obtain income from two or more sources within two (or more) Mainland GBA cities, the subsidies are shared proportionately by the relevant municipal governments.

Details application guidelines and documents required will be announced by each city separately. Taxpayers and employers are suggested to watch out for further announcements made by the authorities as well as application due dates. Note that while some cities offer a second window for late applications, other cities do not.

Points to note

The local implementation rules do bring clarity to those who would qualify for the IIT rebates. However, the rules published to date do not provide answers to the following questions:

Location of employee and employment

It is noted that the definition of “high-end talent” or “talent in short supply” vary among the cities. Therefore, one may qualify for the tax rebate in one Mainland GBA city but not necessarily others. As IIT is normally filed and paid where the withholding agents are located, considering a group of companies with subsidiaries in many Mainland GBA cities, does it mean that the employees would be entitled to IIT rebates as long as their employment/secondment are located in a location where they qualify for a rebate even if their primary working locations is not in that city? While some Mainland GBA cities, e.g. Guangzhou requires the IIT rebate applicants to stay in the city for at least 90 days during a tax year, this is not something unachievable if the working locations of the employees are only of secondary importance to their job.

Application of general anti-avoidance rules

Considering the case above, will tax bureaus use the newly introduced general anti-avoidance rules in counteracting these arrangements?

Individuals changing employment

According to the indicative IIT rebate procedures, the withholding agents are preferably the parties handling the applications and collections of the IIT rebates for taxpayers. Consider the case of individuals changing jobs during a tax year or leaving Mainland China. Would it be practically possible for the individuals to apply for the IIT rebate themselves or apply for the IIT rebates before their departure from Mainland China?

Claiming tax credits for Hong Kong salaries tax

For Hong Kong residents, who hold Hong Kong employment and are required to work in other Mainland GBA cities, Section 50 of the Inland Revenue Ordinance (IRO) allows them to claim tax credits against their Hong Kong salaries tax liabilities. This is a means to fully or partially eliminate double taxation in the two tax jurisdictions. According to Section 50AA(6) of the IRO, the Inland Revenue Department (IRD) is authorized to issue additional assessments when the amount of relief from double taxation given to taxpayers becomes excessive. If the IIT rebate is considered as a financial subsidy but not a refund of IIT paid, it is arguable that the IIT rebate should not affect double taxation relief of the individuals. This position is subject to the IRD’s agreement, and we would expect further clarification by the IRD and sharing of practical experiences with similar financial subsidies from other jurisdictions, if any.

Conclusion

The IIT rebate could bring a significant competitive advantage for talent acquisition in the Mainland GBA cities. While the level of IIT rebate is attractive, its impact will depend on the range of beneficiary groups. As of 17 September, Shenzhen, as one of the four growth engine cities in the GBA, has not yet published their local rules and implementation measures. Meanwhile, businesses should analyse the background and qualifications of their employees and estimate their potential tax savings. To take full advantage of the IIT rebate policy, businesses may consider revisiting their talent deployment strategy. For example, centralizing functions by deploying expatriate employees who are classified as “high-end talent” or “talent in short supply” to one of the Mainland GBA cities.

Once the eligible employees are identified, proper travel schedules should be maintained by the employees to ensure that they meet the specific thresholds for applying the IIT rebate.

The IIT rebate would be distributed to the personal account of the applicants after the application is approved. If eligible employees are covered under a tax equalization arrangement, employees may have to refund the IIT rebate to the employer. For these cases, employers should communicate with the employees and revisit their existing tax equalization policies and arrangements to ensure proper refund of the rebate.

The IIT rebate is good news for foreigners and Hong Kong, Macau and Taiwan residents, as well as some qualified Chinese nationals who plan to work in the Mainland GBA cities. In order to secure this IIT rebate, it is important for both businesses and individuals to stay abreast of the policy updates and implementation details. The involvement of multiple government bodies could potentially be a challenge for applicants. Where possible, professional advisors should be involved in the application process.

This article is contributed by Mona Mak, Partner, and Kenneth Peh, Tax Director, of Deloitte Advisory (Hong Kong).